Post-war Ukraine: Outperformance, outperformance & outperformance

Deep dive on Ukrainian markets - Where are the best investing opportunities?

“Biggest Opportunity in Europe since World War II”

—Volomydyr Zelenskyi, President of Ukraine

Since the Kosovo War ended in June 1999 after a major bombing campaing by NATO, there has not been a full-scale war fought in European soil. However, that long lasting peace came into an end in February 2022, after Russia started a full-scale invasion in Eastern Ukraine, claiming it to be 3-day special operation.

As we close year 2025 in few weeks time, that 3-day special operation has extended into 1385 days, 46 months or 197 weeks and there is still no clear resolution in sight, although the year of 2025 brought a lot of hope for many following the election of Donald Trump.

In this article, I will dive into Ukrainian markets and introduce you to 17 companies that either operates in Ukraine or can benefit significantly when/if the peace is eventually reached.

Disclaimer

I am not a war expert, and I do not make any predictions in this article about when the situation in Ukraine might change for the better. This article only discusses companies that either have operations in Ukraine or could significantly benefit from the end of the war. There is no guarantee that all the companies mentioned in the article will be able to continue their operations as normal if/when the war continues to go on.

This article is structured as follows;

Glimpse of market behaviour around both positive and negative sentiment followed by a dedicated segment to the companies. I go through all 17 companies very briefly, as I intend to keep this article in readable length. The goal is to highlight some key points and red flags about every company and give you some inspiration to conduct your own deeper research.

Companies mentioned in this article;

Finnair, Black Iron, Kyivstar, Enwell Energy, MLK Foods Public, Agroton, Astarta Holding, Cadogan Energy, Ferrexpo, IMC, Budimex SA, Kernel Holding SA, KSG Agro SA, MHP, Mirbud SA, Unibep, Ukrproduct.

What we can learn from the markets

“In the short-term, stock market is a voting machine”

Benjamin Graham said it perfectly. As a long term investor, I don’t care about short term price movements too much, but in certain situations it makes perfect sense to choose the same companies that the market generally likes.

This has nothing to do with quality companies and long term investing, but when we make a swing trades based on a specific catalyst, studying market behaviour before-hand can be a difference between making a lot of money and collecting pennies. You absolutely want to pick up a company that has the highest beta against its peers who have the same catalyst, even if that means the company is not best in-class. Market rarely rewards companies, that would fundamentally benefit most from the catalyst. Trying to be too smart on short term swing trading is usually a bad idea—just go with a market darling.

This has nothing to do with quality companies or long-term investing, but when we swing trade based on a particular catalyst, studying the market behaviour beforehand can be the difference between making big money and collecting pennies. You definitely want to pick the company with the highest beta compared to its competitors with the same catalyst, even if that means the company isn’t fundamentally best in class. The market rarely rewards the companies that would fundamentally benefit the most from the catalyst. Trying to be too smart in short-term swing trading is usually a bad idea – just pick the market darling.

That is why I wanted to add the market behaviour segment into the article.*

*Kyivstar is absent from all Case Studies as the company IPO’ed only couple months ago, in August 2025.

Case Study #1 - Negative Market Sentiment

I have picked few examples to monitor negative market sentiment.

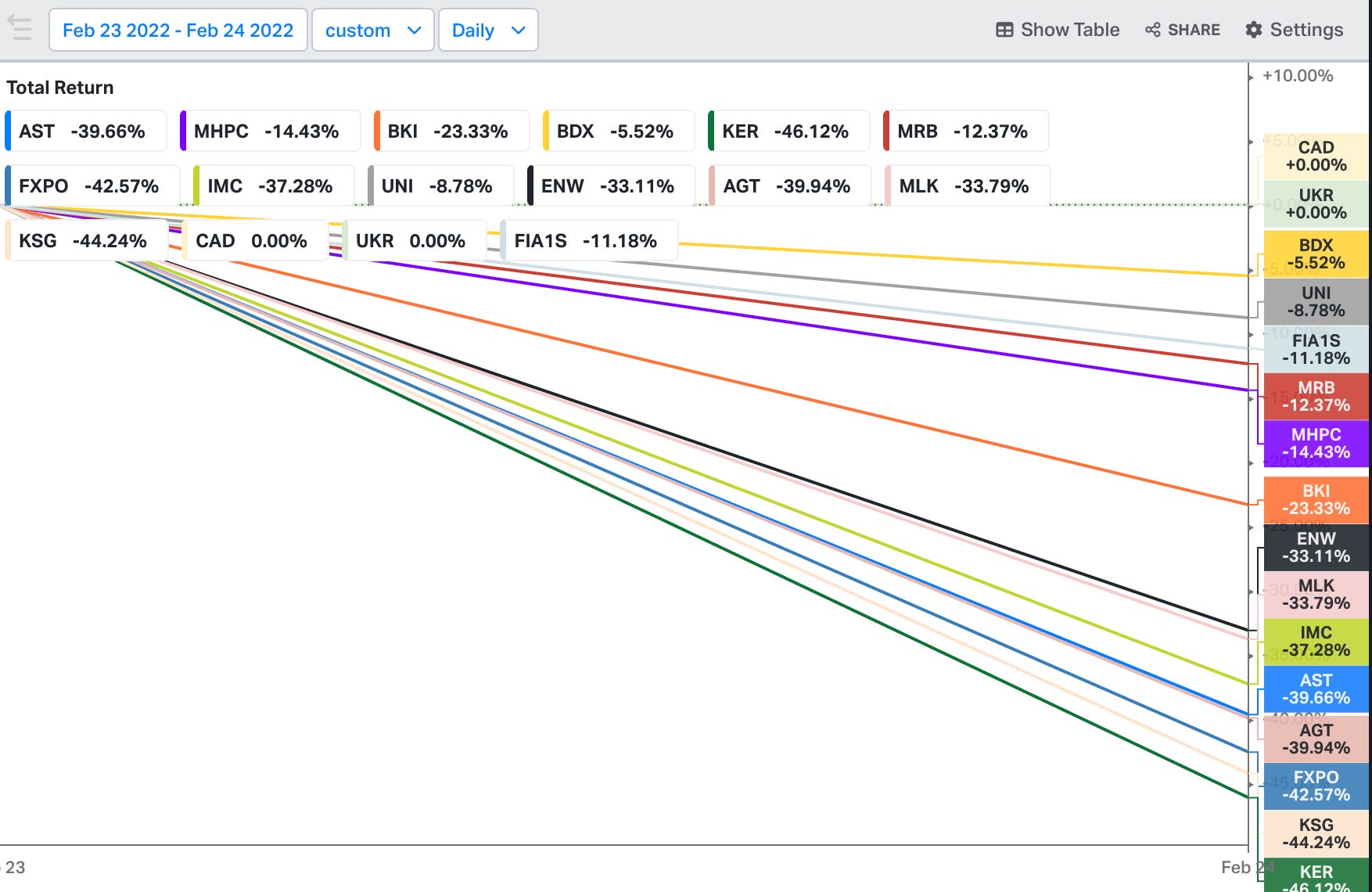

Example 1: February 23, 2022 - February 24, 2022 - Full scale invasion begins

What I love about timeframe this tight is that it shows pure emotions of the investors. There is no time to assess the situation, just pure panic and uncertainty about the future. Russia is claiming that their “special operation” will take only 3 days and nobody knows yet what is going to happen to the Ukrainian companies. As expected, the share prices declined significantly in this 2 day period, when the full scale war officially started.

Companies from worst to best in this timeframe (February 23, 2022 - February 24, 2022):

Kernel Holdings (KER) -46.12%

KSG Agro (KSG) -44.24%

Ferrexpo (FXPO) -42.57%

Agroton Public Limited (AGT) -39.94%

Astarta Holdings (AST) -39.66%

IMC S.A (IMC) -37.28%

MLK Foods PLC (MLK) -33.79%

Enwell Energy (ENW) -33.11%

Black Iron (BKI) -23.33%

MHP SE (MHPC) -14.43%

Mirbud (MRB) -12.37%

Finnair (FIA1S) -11.18%

Unibep S.A (UNI). -8.78%

Budimex (BDX) -5.52%

Ukrproduct (UKR) 0.00%

Cadogan Energy (CAD) 0.00%

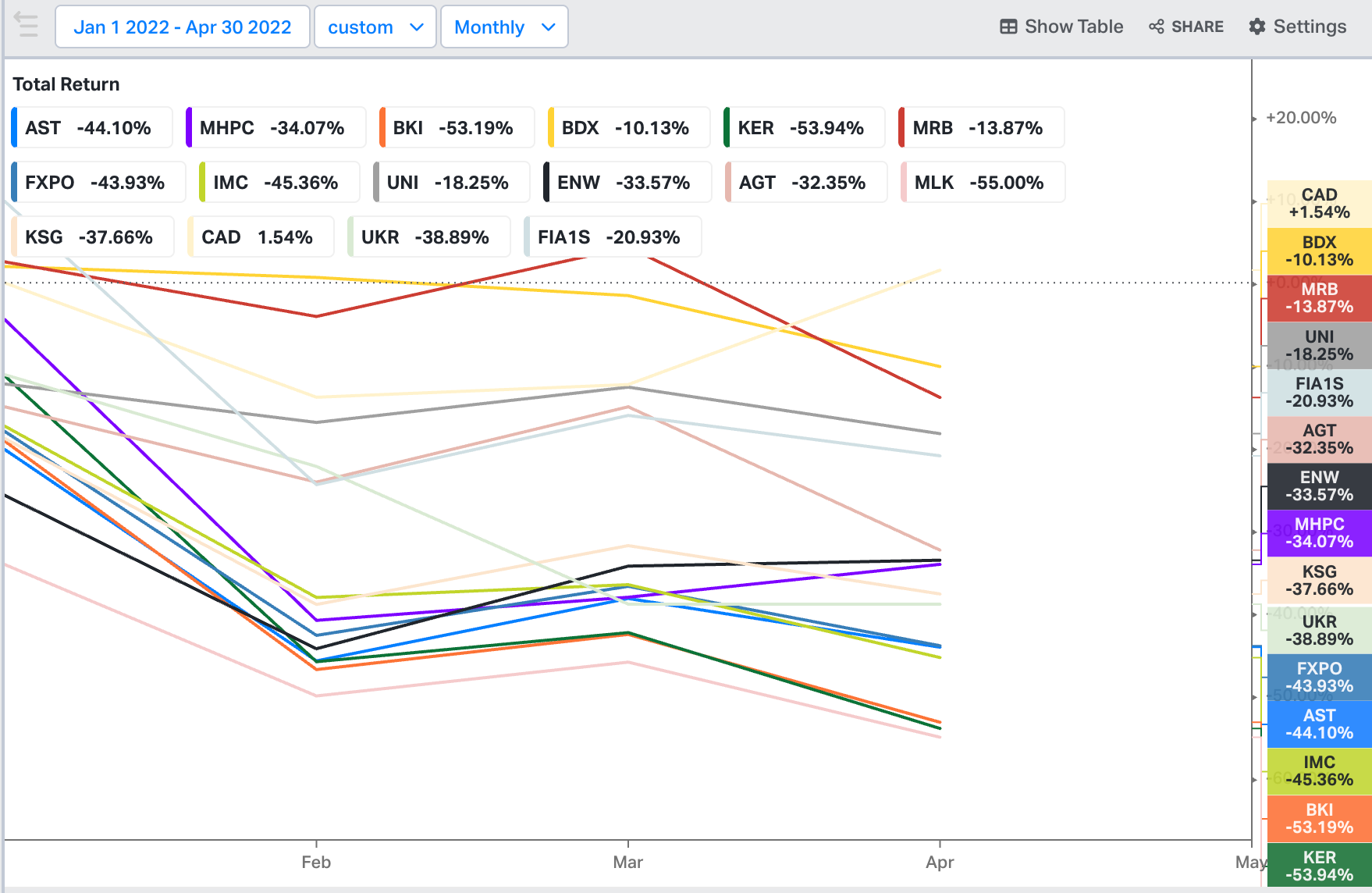

Example 2: January 1, 2022 - April 30, 2022 - From rumours to reality

This timeframe is longer; Four full months from January 1, 2022 to April 30, 2022. Many people consider that after all the full-scale war was a surprise, but in January 2022 we started to have extensive intel information that the attack might prevail soon. And as you probably know, the market usually tends to react heavily into rumours.

It is also important to note that in this 4 month timeframe these companies might have had some internal, not-war-related issues, so beware of that. I didn’t go through the every company and their press releases, so this is pure share price performance without additional context behind that. However the trend is clear; heavily down.

Companies from worst to best in this timeframe (Jan 1, 2022 - April 30, 2022):

MLK Foods PLC (MLK) -55.00%

Kernel Holdings (KER) -53.94%

Black Iron (BKI) -53.19%

IMC S.A (IMC) -45.36%

Astarta Holdings (AST) -44.10%

Ferrexpo (FXPO) -43.93%

Ukrproduct (UKR) -38.89%

KSG Agro (KSG) -37.66%

MHP SE (MHPC) -34.07%

Enwell Energy (ENW) -33.57%

Agroton Public Limited (AGT) -32.35%

Finnair (FIA1S) -20.93%

Unibep S.A (UNI). -18.25%

Mirbud (MRB) -13.87%

Budimex (BDX) -10.13%

Cadogan Energy (CAD) +1.54%

It is important to note that in this 4 month timeframe these companies might have had some internal, not-war-related issues, so beware of that. I didn’t go through the every company and their press releases, so this is pure share price performance without additional context behind that. However the trend is clear; heavily down.

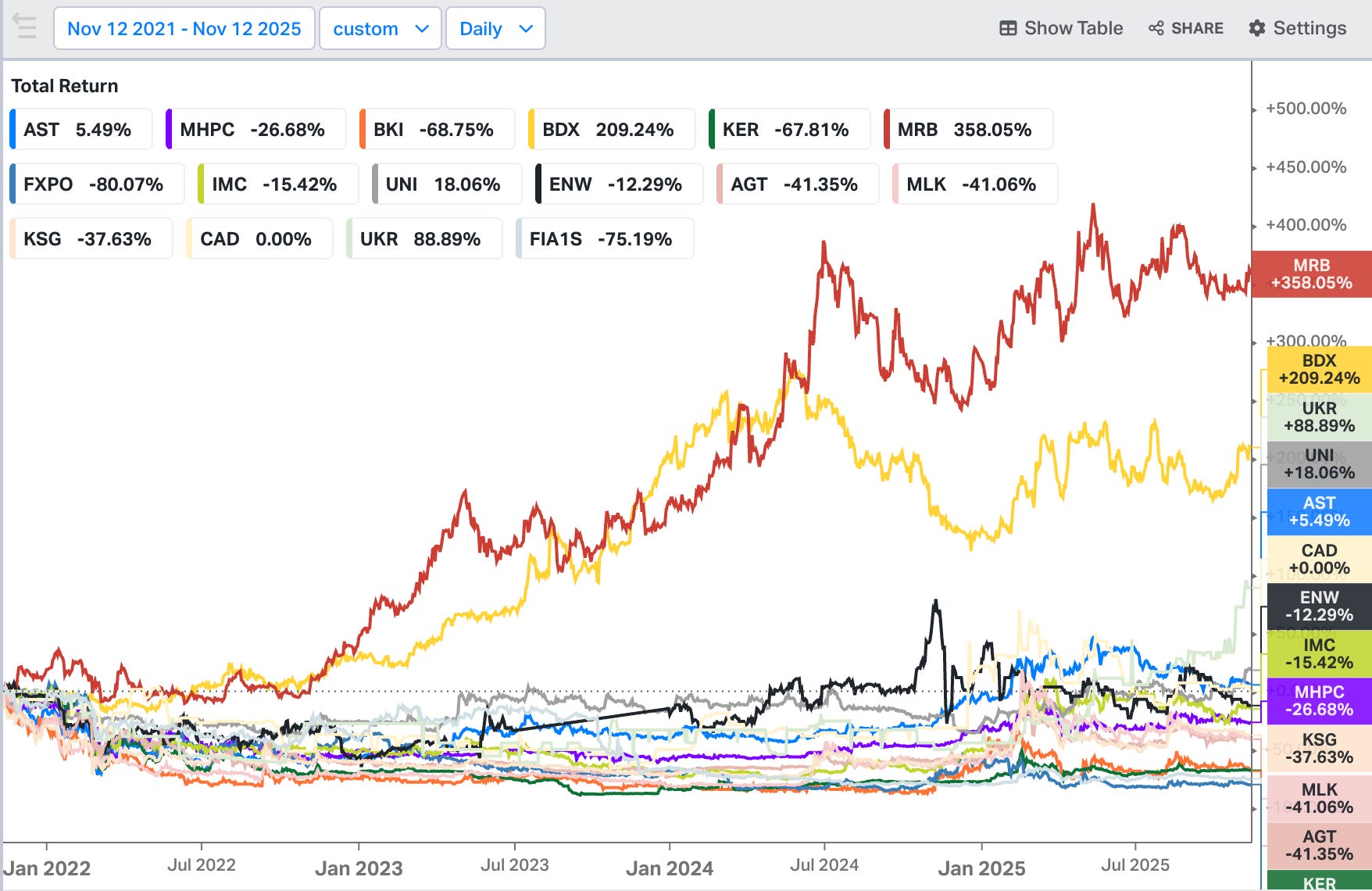

Example 3: Nov 12, 2021 - November 12, 2025 - Equity performance over the lengthy war

Next timeframe is the longest, stretching from November 2021 to November 2025. This basically includes it all; From initial rumours about full-scale war to this date. There we are already seeing massive divergence between peers like Astarta and Kernel Holdings, which both operate in Agricultural sector. While Astarta has achieved positive nominal returns over the timeframe, Kernel Holdings have dropped roughly 70% from November 2021 levels.

Note: Mirbud (MRB), Budimex (BDX) and Unibep (Uni) are Polish constructor companies that have been historically active in Ukraine or have signed LOIs or MOUs to participate in the re-construction of the country. If you are wondering about the outperformance, the war has not affected their core business as much as it has affected Ukrainian companies. In the other hand, Ukrproduct (UKR) has shown amazing outperformance and resilience given its strong presence in a war-riddled country.

Companies from worst to best in this timeframe (Nov 12, 2021 - Nov 12, 2025):

Ferrexpo (FXPO) -80.07%

Finnair (FIA1S) -75.19%

Black Iron (BKI) -68.75%

Kernel Holdings (KER) -67.81%

Agroton Public Limited (AGT) -41.35%

MLK Foods PLC (MLK) -41.06%

KSG Agro (KSG) -37.63%

MHP SE (MHPC) -26.68%

IMC S.A (IMC) -15.42%

Enwell Energy (ENW) -12.29%

Cadogan Energy (CAD) 0.00%

Astarta Holdings (AST) +5.49%

Unibep S.A (UNI). +18.06%

Ukrproduct (UKR) +88.89%

Budimex (BDX) +209.24%

Mirbud (MRB) +358.05%

Case Study #2 - Positive Market Sentiment

We always want to study both sides of the coin, so I have created few examples of positive market sentiment as well. Most of us are here to make money, so its important to understand which companies are the market darlings.

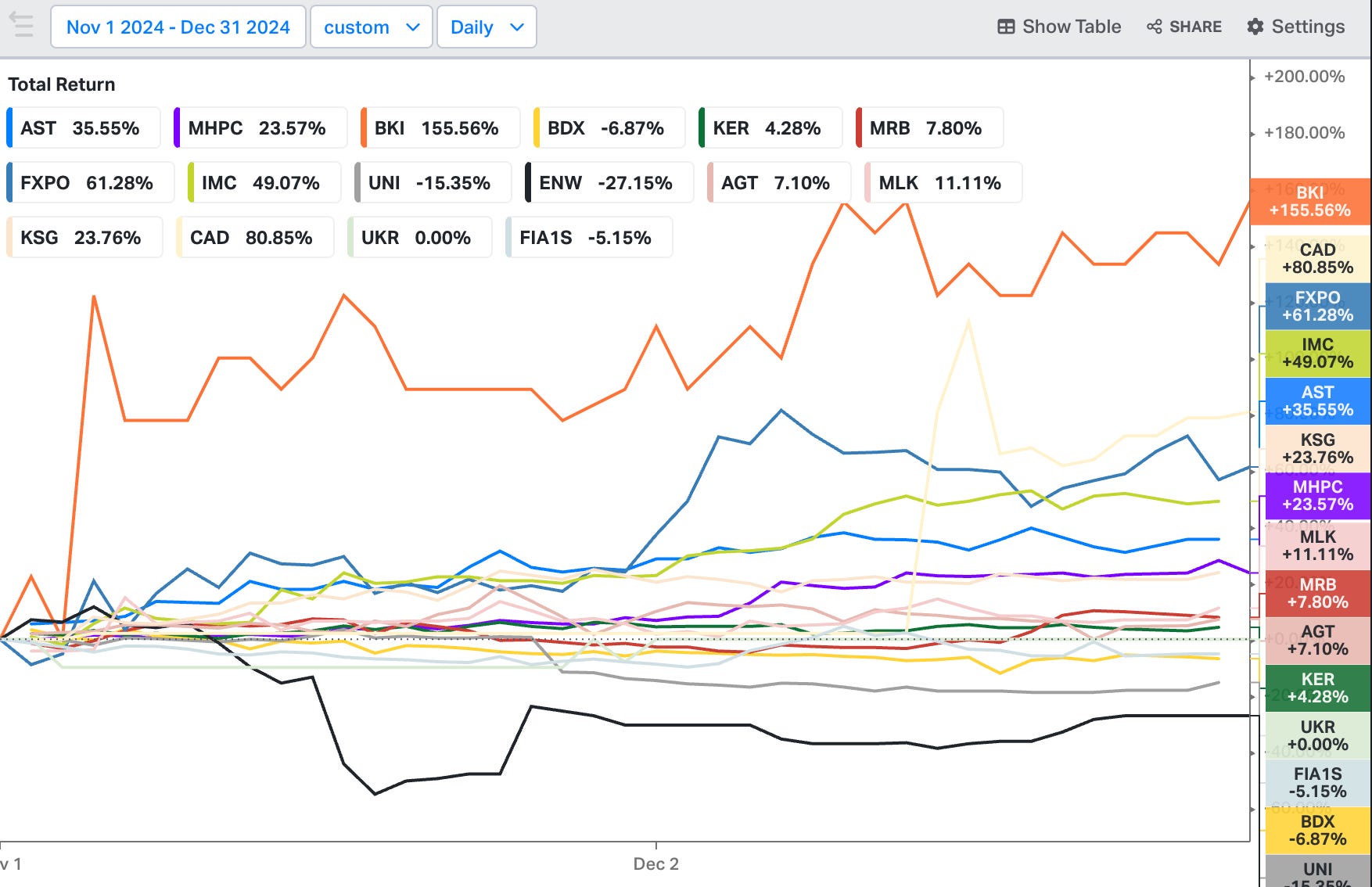

Example 1: November 1, 2024 - December 31, 2024 - Donald Trump takes the office

Donald Trump being elected as POTUS47 sparked a little glimmer of hope into Ukrainian stocks, as the now two time president had strongly suggested that under his reign the war would come to an end relatively quick. The market certainly believed that, as we can see below how much the stocks rallied during his first 2 months in the office.

Companies from best to worst during this timeframe (Nov 1, 2024 - Dec 31, 2024):

Black Iron (BKI) +155.56%

Cadogan Energy (CAD) +80.85%

Ferrexpo (FXPO) +61.28%

IMC S.A (IMC) +49.07%

Astarta Holdings (AST) +35.55%

KSG Agro (KSG) +23.76%

MHP SE (MHPC) +23.57%

MLK Foods PLC (MLK) +11.11%

Mirbud (MRB) +7.80%

Agroton Public Limited (AGT) +7.10%

Kernel Holdings (KER) +4.28%

Ukrproduct (UKR) 0.00%

Finnair (FIA1S) -5.15%

Budimex (BDX) -6.87%

Unibep S.A (UNI) -15.35%

Enwell Energy (ENW) -27.15%

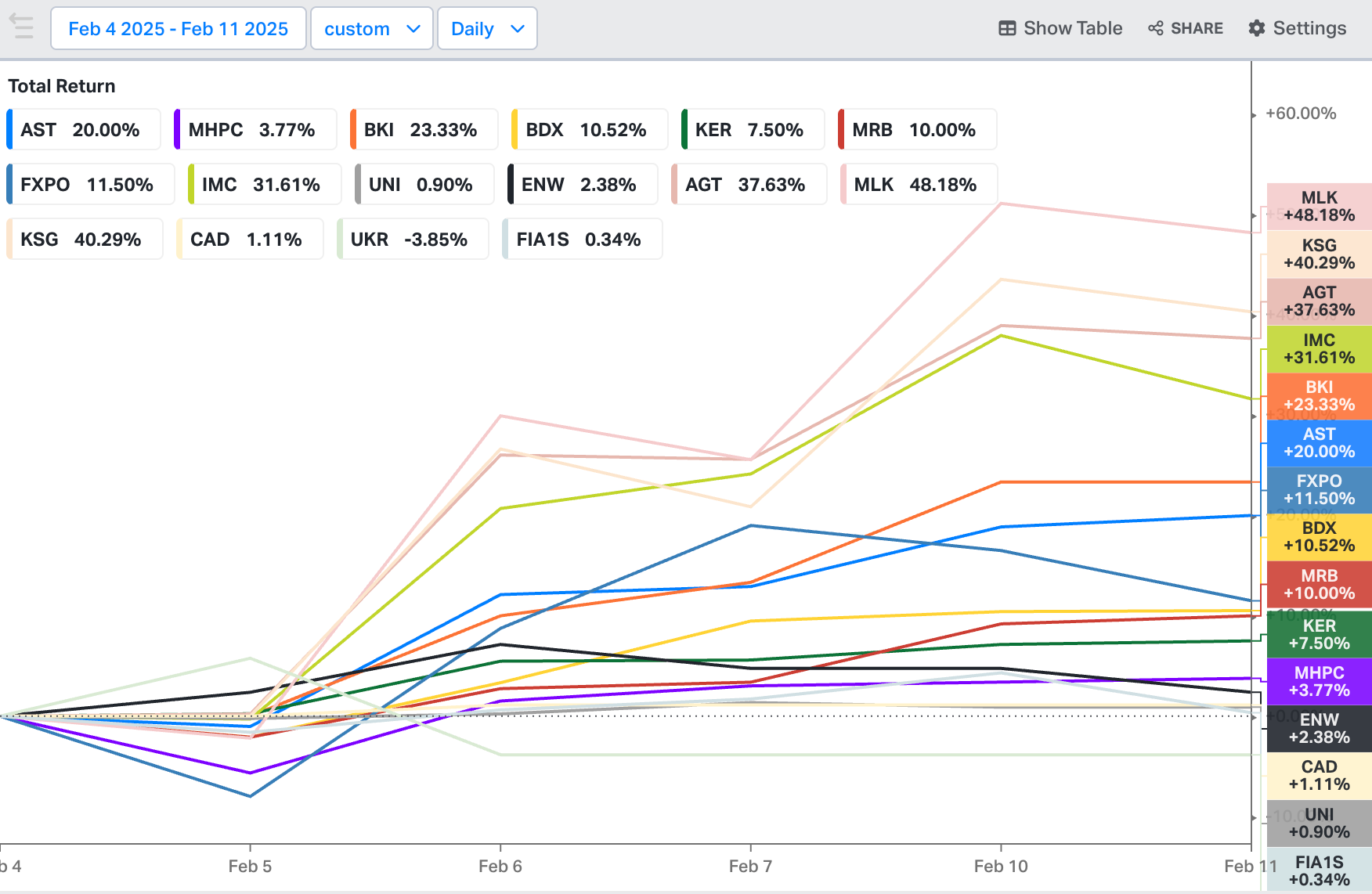

Example 2: February 4, 2025 - February 11, 2025 - Trump-Putin agree to negotiate

In February 12th 2025, Donald Trump and Vladimir Putin agreed to negotiate to find a solution in to Russia-Ukraine war. The week before that the rumours increased and the stocks rallied due optimism surrounding the direct negotiations. The talks sadly sadly ended without a solution.

However, this offered us one more opportunity to gather data and study market behaviour regarding the possible peace agreement in the future. Interestingly enough in this short timeframe the Agricultural and Food Industry companies outperformed the field significantly, with MLK Foods leading the pack with impressive gains of 48% over only five trading sessions.

Companies from best to worst during this timeframe (Feb 4, 2025 - Feb 11, 2025):

MLK Foods PLC (MLK) +48.18%

KSG Agro (KSG) +40.29%

Agroton Public Limited (AGT) +37.63%

IMC S.A (IMC) +31.61%

Black Iron (BKI) +23.33%

Astarta Holdings (AST) +20.00%

Ferrexpo (FXPO) +11.50%

Budimex (BDX) +10.52%

Mirbud (MRB) +10.00%

Kernel Holdings (KER) +7.50%

MHP SE (MHPC) +3.77%

Enwell Energy (ENW) +2.38%

Cadogan Energy (CAD) +1.11%

Unibep S.A (UNI) +0.90%

Finnair (FIA1S) +0.34%

Ukrproduct (UKR) -3.85%

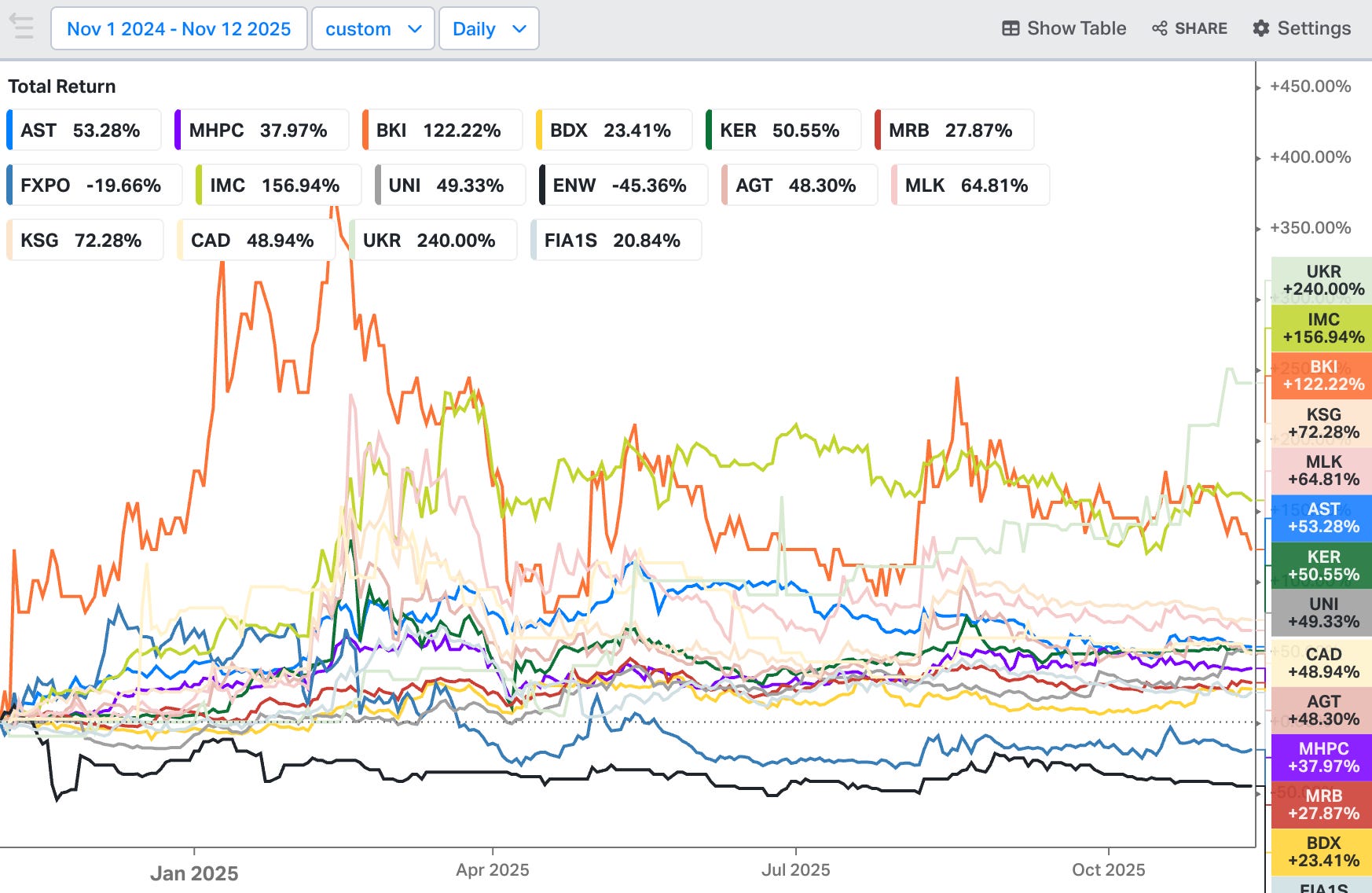

Example 3: November 1, 2024 - November 12, 2025 - Trump’s term so far

Since Trump taking the office, every stock except Ferrexpo and Enwell Energy (Understandably so, more on that on company specific segment) on my Ukraine watchlist have outperformed S&P500. Despite the high hopes of the market, we haven’t been able to reach the peace agreement that would put this war into the end. I personally feel that we are closer to peace than anytime during Biden’s term, but as I said in the beginning, I’m not a war expert so don’t take my opinion as something that holds weighting regarding this topic.

Whether you believe me, the market, President Trump or somebody else, one thing is clear; Ukraine basket have performed beautifully during the last 12 months. Three companies have at least doubled and the top performer, Ukrproduct, have achieved impressive 3.4x returns.

Companies from best to worst during this timeframe (Nov 1, 2024 - Nov 12, 2025):

Ukrproduct (UKR) +240.00%

IMC S.A (IMC) +156.94%

Black Iron (BKI) +122.22%

KSG Agro (KSG) 72.28%

MLK Foods PLC (MLK) +64.81%

Astarta Holdings (AST) +53.28%

Kernel Holdings (KER) +50.55%

Unibep S.A (UNI) +49.33%

Cadogan Energy (CAD) +48.94%

Agroton Public Limited (AGT) +48.30%

MHP SE (MHPC) +37.97%

Mirbud (MRB) +27.87%

Budimex (BDX) +23.41%

Finnair (FIA1S) +20.84%

Ferrexpo (FXPO) -19.66%

Enwell Energy (ENW) -45.36%

Companies Briefly

Now that we know what the market thinks and how it behaves, let’s take a quick look on the companies as well. These are not deep dives by any means—only a small glance behind the curtains. The goal is not to give you any investment advices, but to hopefully give you couple interesting ideas which you can research more and make sure you have your strategy in place when/if the war eventually ends.

I tried to highlight the most obvious red flags, but my research on most these companies has been very limited, so please conduct your own due diligence on top of these readings.

There are in total of 17 companies from 7 different sectors, (Agriculture, food industry, telecommunications, mining, energy, constructing, travel industry) so lets get into it!

Agriculture

Agriculture is a huge part of Ukraine’s export economy. And that is no wonder, as Ukraine’s soil is among the best suited for farming in the world. Among the top ten companies in the sector are three companies mentioned in this article, with Kernel Holdings being the 2023 revenue king. Also, from the 17 companies in this article, 6 are agricultural businesses.

Kernel Holdings (WSE:KER)

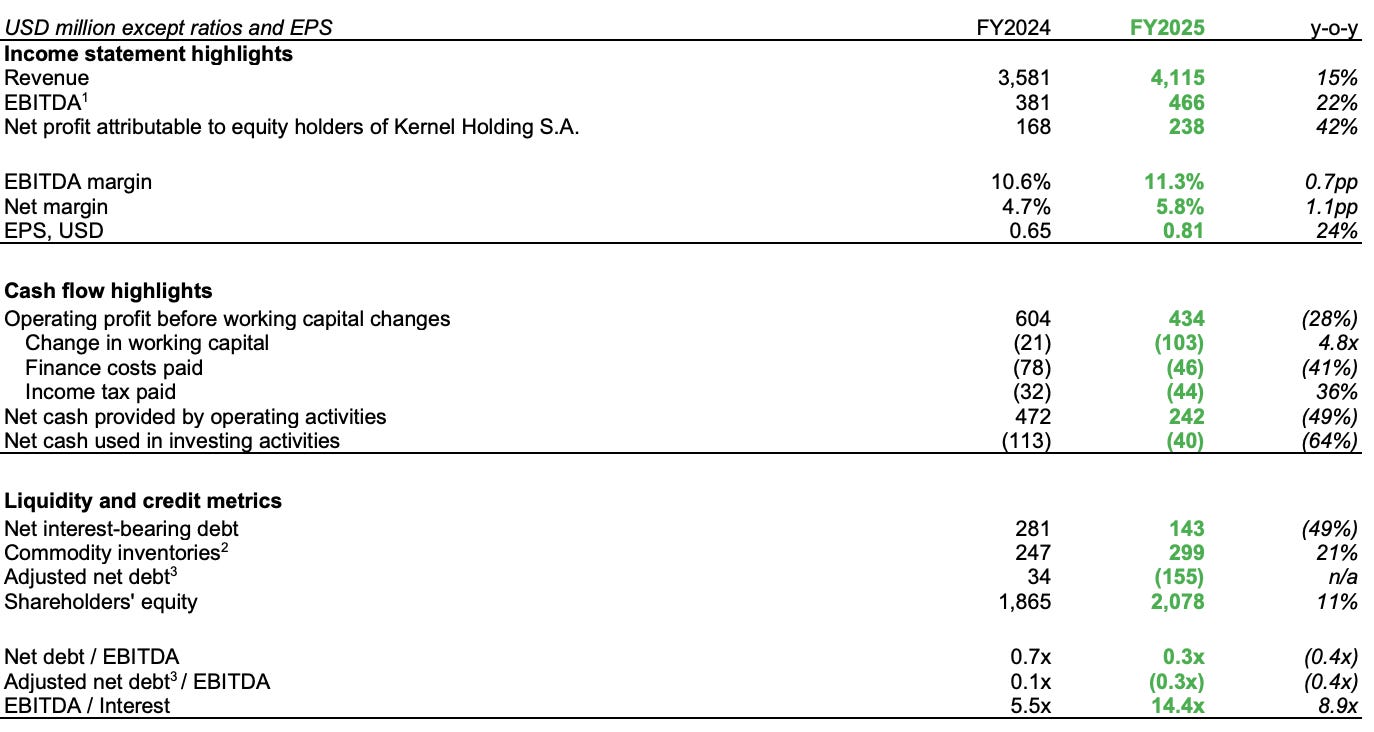

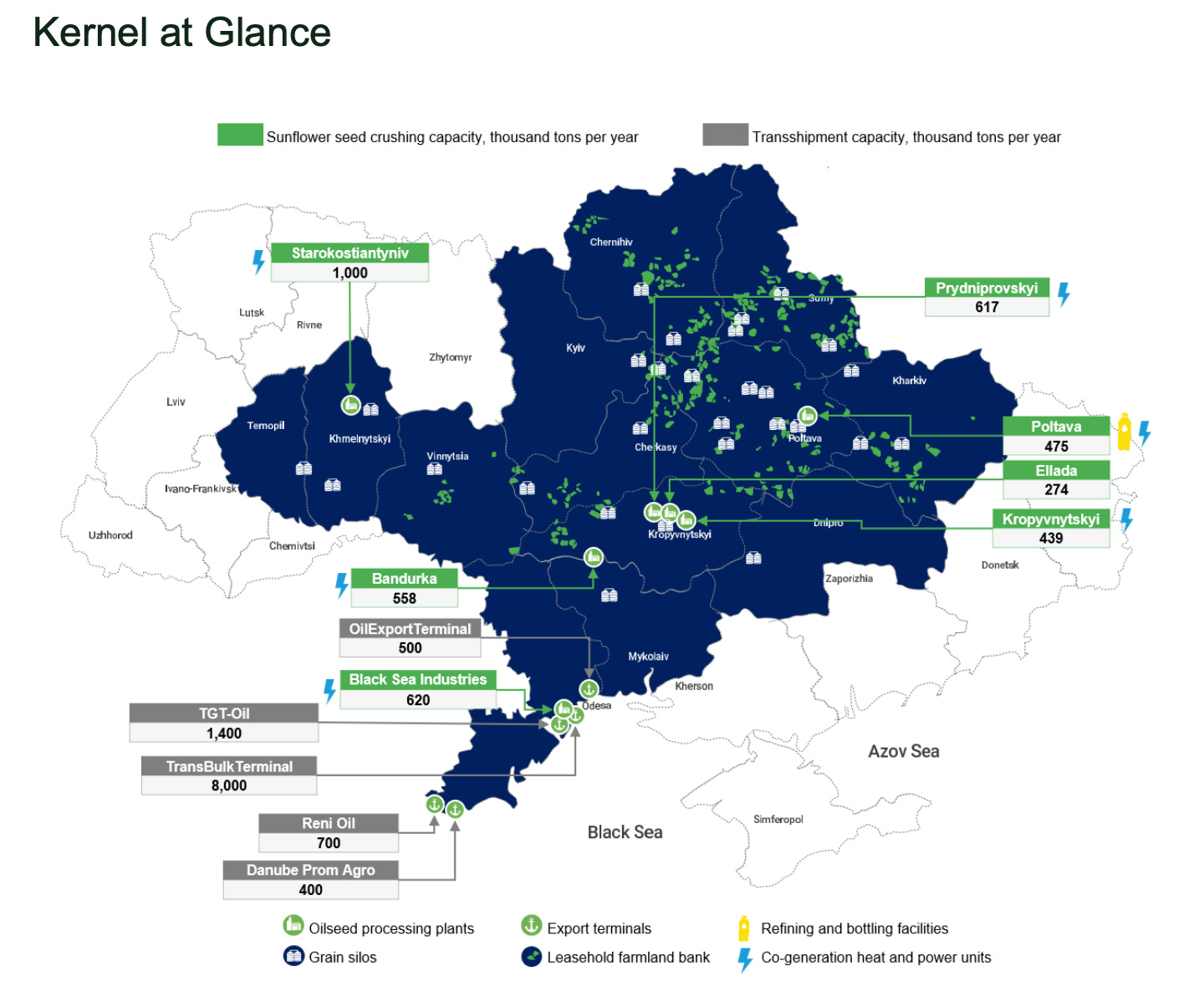

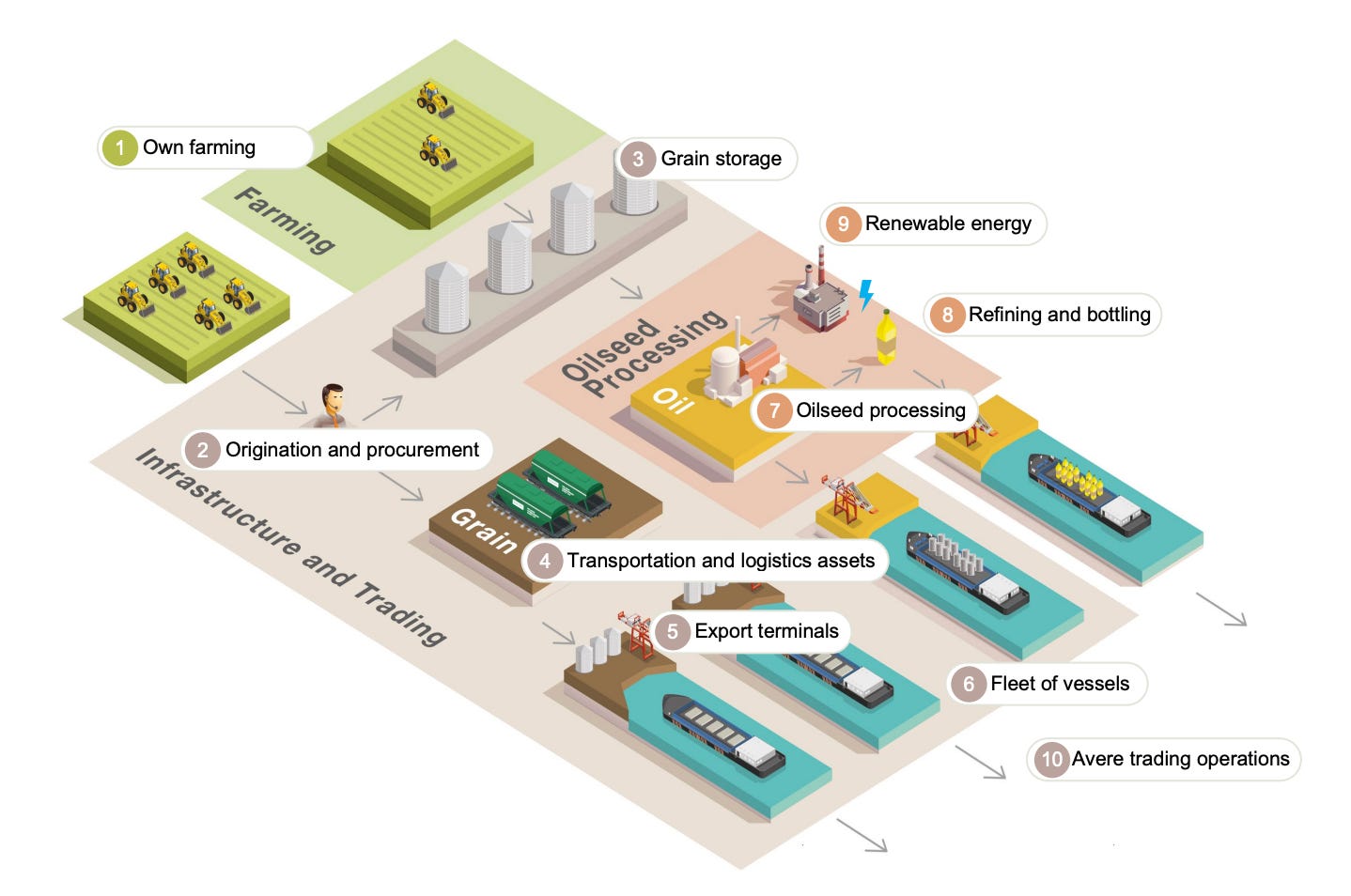

Kernel is Ukraine’s largest grain producer and exporter, a leader in the global sunflower oil market and a major supplier of agricultural products from the Black Sea region to international markets. The company accounts for approximately 8% of global sunflower oil exports. Kernel supplies its products to over 60 countries.

Fitch Ratings upgraded its credit rating to CC- from CCC- at the end of 2024. Although CCC- still indicates high credit risk, Kernel has been able to achieve solid financial performance and the company even fully redeemed its US$300 million Eurobonds that matured on October 17, 2024.

After its revenue decreased from US$5,332 million (FY2022) to US$3,455 million (FY2023) due to the full-scale attack, Kernel has been able to increase its revenue in FY2024 and FY2025, while also maintaining profitability.

Kernel has important infrastructure near the front lines in eastern Ukraine, but so far the company has been able to use several ports connecting Ukraine to the Black Sea without significant problems.

MHP (LSE:MHPC)

MHP is the largest integrated producer and exporter of poultry and grain, as well as other meat, sausage and finished meat products in Ukraine. The company is the actually one of the leading poultry producers in Europe, with one of the strongest food brands in Ukraine, producing about 700 thousand tons per year. MHP exports its products to more than 70 different countries.

MHP has a significant economic importance in Ukraine, as it has been the largest taxpayer in the agricultural sector for several consecutive years, and during the war years in 2022-2024, the company paid 18.2 billion Ukrainian hryvnias (430 million US dollars) in taxes and fees. In addition, the company has invested about 690 million US dollars in business development in 2022-2024.

Like Kernel, MHP has recovered and actually increased its revenue year-over-year during the ongoing war;

2022 - US$2.641 million

2023 - US$3.021 million

2024 - US$3.046 million

A quick look at the financial numbers suggests that MHP has a very good chance of surviving this dark period. A prolonged war would certainly do no good, but it is impressive how well these agricultural giants are holding their businesses together.

Some brands from MHP. I, a Finnish guy can’t recognise any one of them.

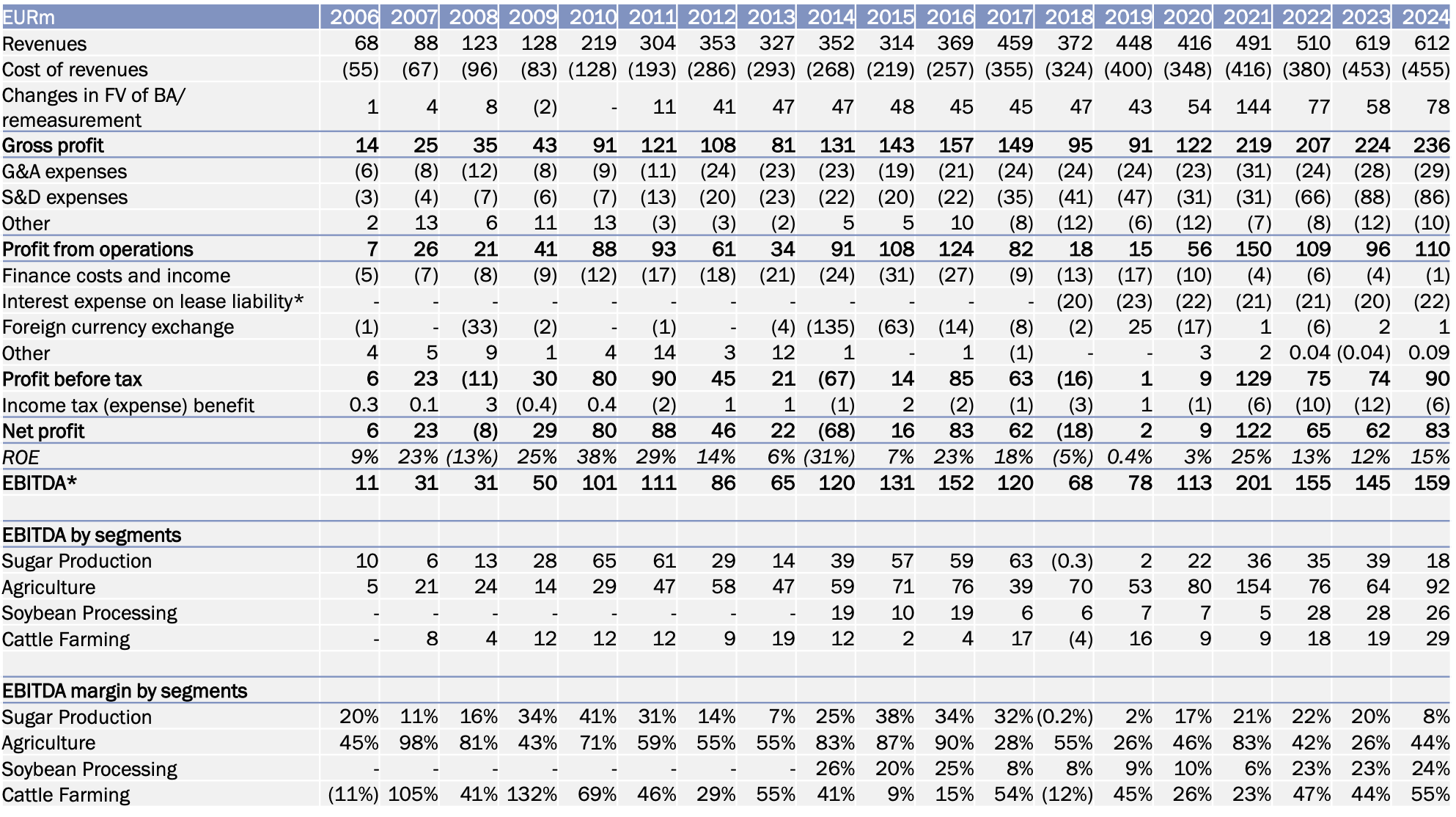

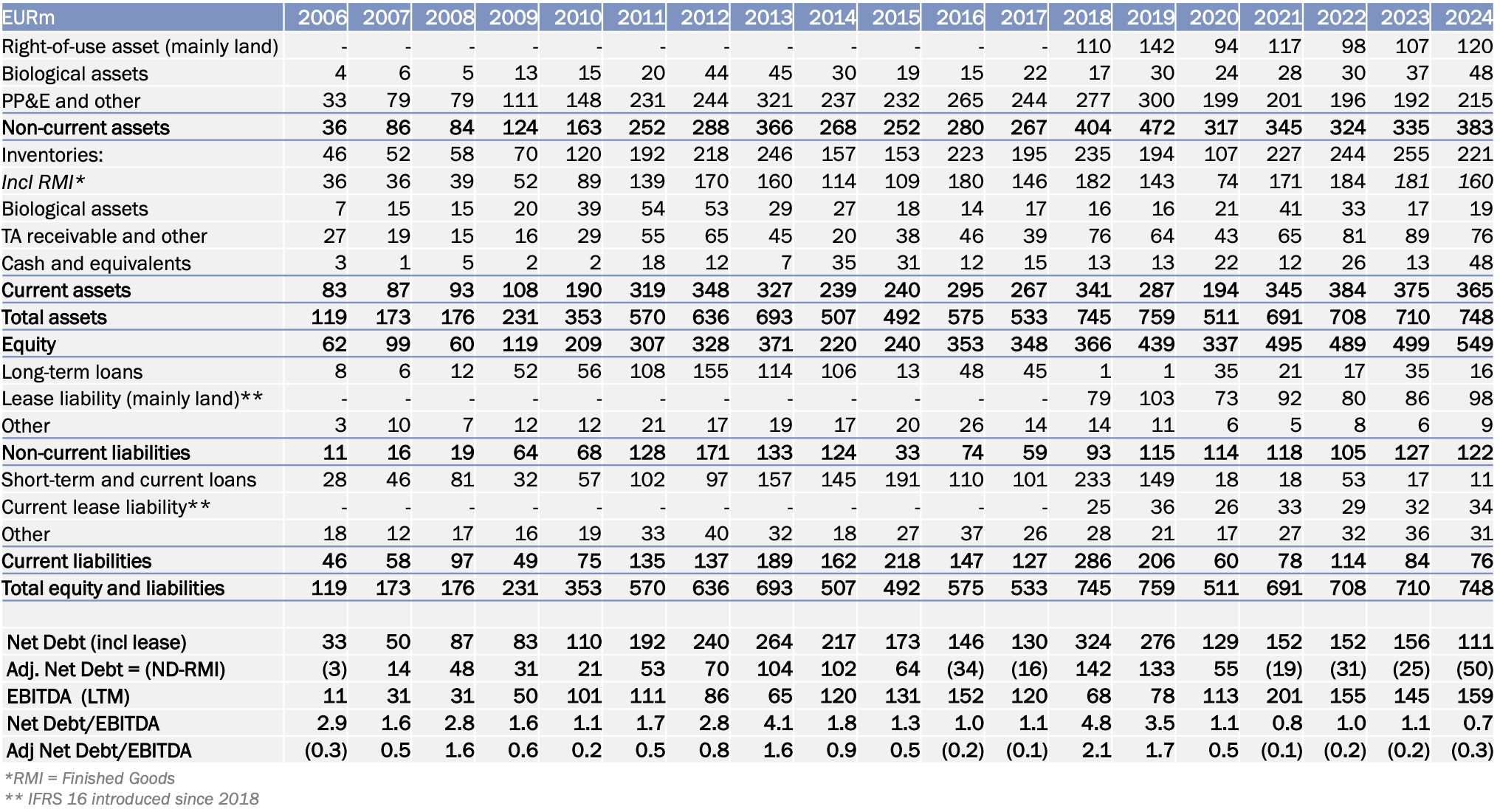

Astarta Holding N.V (WSE:ASTH)

Astarta Holding is the largest sugar producer in Ukraine, with an annual sugar production of 250,000–500,000 tons. In addition, the company produces 230,000 tons of soybeans and 119,000 tons of milk, which also makes it largest of its kind in Ukraine. If you are wondering how many cows the largest dairy producer in Ukraine has, the answer is 29,000. That is a lot of moo’ing.

In terms of revenues, Astarta has grown steadily since 2006, and in recent years the trend has been mainly upward despite the war and coronavirus. Astarta is still a relatively small player in Ukrainian agricultural sector compared to the two giants (Kernel, MHP), but who knows what the future holds. With 29,000 cows (and growing), anything is definitely possible.

No issues with liabilities either; During the 18-year period the Net Debt/EBITDA has stayed well under control and its currently at its lowest point during the period.

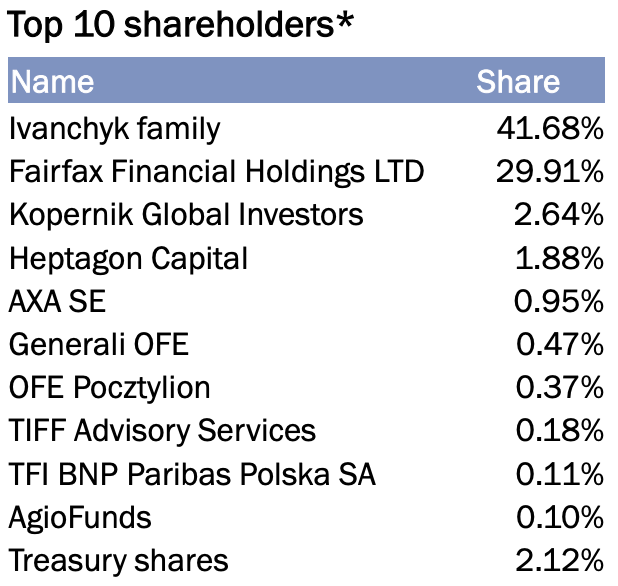

An interesting detail: Astarta’s shareholder structure is highly concentrated, with the two largest shareholders owning over 71.5% of the shares. Viktor Ivanchyk, whose family owns 41.68% of the shares, is also the founder of the company.

IMC SA (WSE:IMC)

IMC is one of the ten largest agricultural companies in Ukraine, managing 120,000 hectares of fields in key agricultural regions of Ukraine, such as Poltava, Chernihiv and Sumy. IMC has a market share of 5-10% in certain grain types. Of IMC’s 116 hectares of fields, corn dominates the business with a share of 65.1 hectares. The remaining farmland is as follows: 24.8 hectares of sunflower oil, 20.7 hectares of wheat and 5.4 hectares of fallow land.

IMC’s operations are mainly concentrated in the northern part of Ukraine. The nearest active battlefields are in the neighboring regions of Kharkiv and Dnipro. As I write this, Russian army has not occupied Kharkiv or Dnipro, although there is intense fighting in the area.

IMC has achieved steady revenue growth over the past decades. Since the aftermath of the global financial crisis in 2009, the company has grown its revenue more than tenfold. That annual revenue of around $200 million is nothing compared to the big players in the industry, but at least IMC has shown resilience during the past few difficult years.

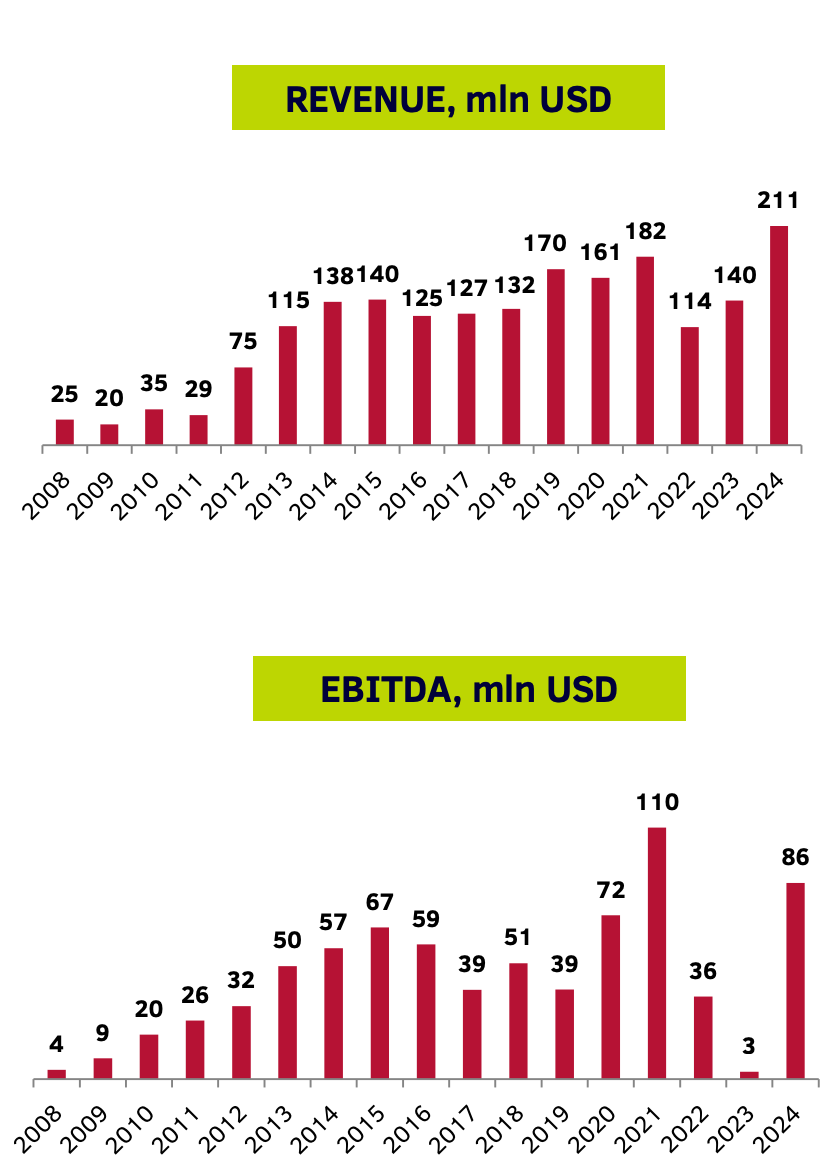

KSG-Agro (WSE:KSG)

KSG Agro is a Luxembourg-based agricultural company that produces grain (corn, wheat, sunflower oil), pigs and other products in Ukraine, Slovakia and Poland. It also provides agricultural services. Its market share is small (about 1-2% in the Ukrainian grain sector), but it is a growing, vertically integrated producer.

KSG-Agro is the smallest agricultural company in Ukraine that made it into my article. With a market capitalization of only $17 million and a market share of about 1.5%, this small company is engaged in grain cultivation, oilseed production and livestock breeding. The company manages over 24,000 hectares of farmland for both grain and oilseed crops.

As I mentioned, the company is also engaged in pig farming and has about 60,000 pigs. KSG-Agro plans to increase this number to 77,000 by 2027 and eventually double the size of its herd to 117,000 heads.

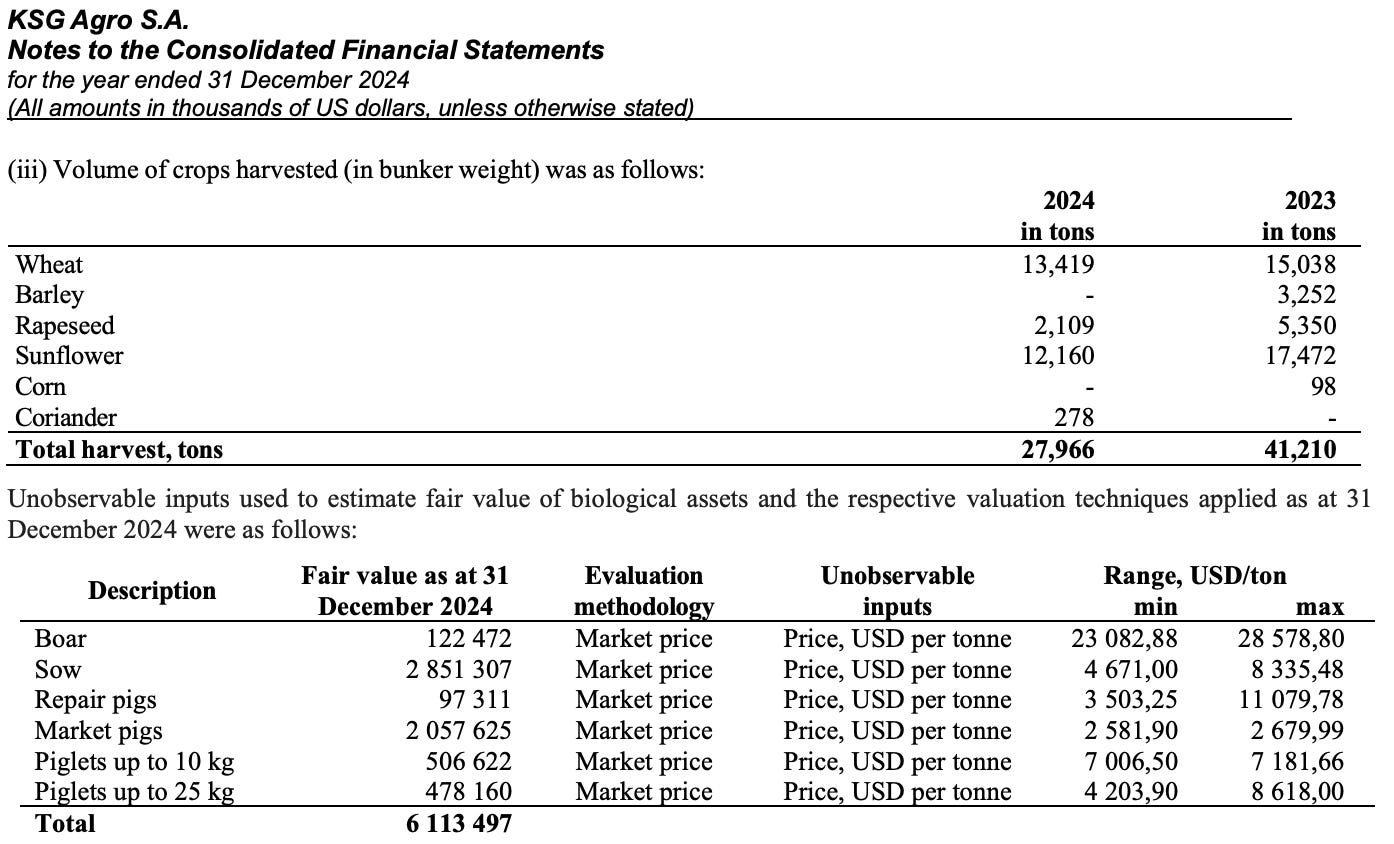

In terms of the agricultural business, the crops harvested in 2024 were mostly wheat and sunflowers, with a small touch of canola and coriander. The company has grown its revenue for three consecutive years, from US$16.2 million in 2022 to US$18.7 million in 2023 and finally to US$22.1 million in 2024.

According to the company, the fair value of the pigs it owns is US$6.1 million as of December 2024. Definitely an interesting detail, as I have never owned or even researched companies that raise and process livestock.

Agroton Public Limited (WSE:AGTP)

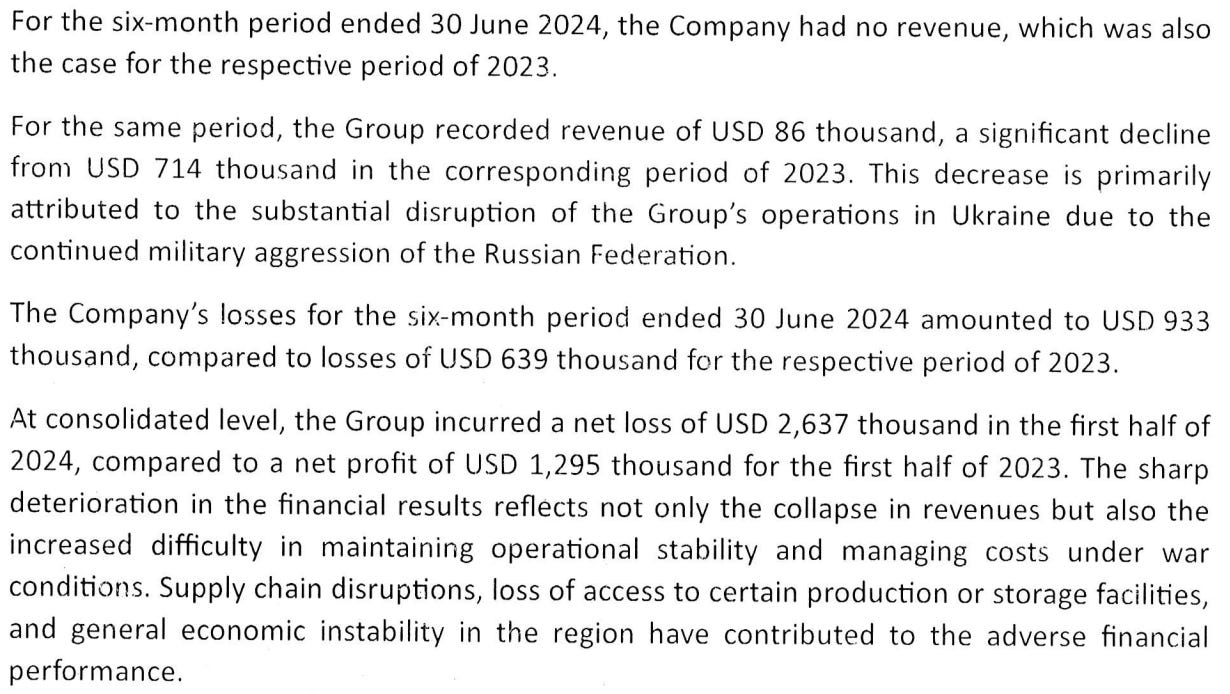

Agroton Public Limited is a crop producer and is likely to be one of the companies most affected by the full-scale war. The company recorded no revenue for the six months ended 30 June 2024, while the group’s total revenue was just $86,000 – a significant drop from $714,000 in the same period in 2023.

At the group level, the net loss was $2,637 million in the first half of 2024, compared to a net profit of $1,295 million in the first half of 2023. That’s not nice. The company also reported difficulties in maintaining overall operational stability in the current situation.

I won’t go into detail about Agroton, as the company is under extreme financial strain as long as the war continues. And if a peace deal is reached, much of the critical infrastructure in eastern Ukraine, where the company primarily operates, has been destroyed. Agroton, once Ukraine’s largest sunflower seed producer that raised $54 million in its IPO in 2010, is probably the first company to fall out of my Ukraine basket.

Food Industry

Mlk Foods Public Company Ltd/Milkiland (WSE:MLK)

MLK Foods is an international dairy producer with its core production assets located in Ukraine. The total annual milk processing capacity exceeds 500 thousand tons.

The company had financial difficulties even before the full-scale invasion and had not reported its financials for years. There is really no point diving in further as the investors are completely blindsided about the financial situation of the company. I’m not legally allowed to give you financial advice, but with this company, I would think twice before even thinking about buying some shares. To be honest, I’m not sure how this company can still have its shares listed without any relevant financial data.

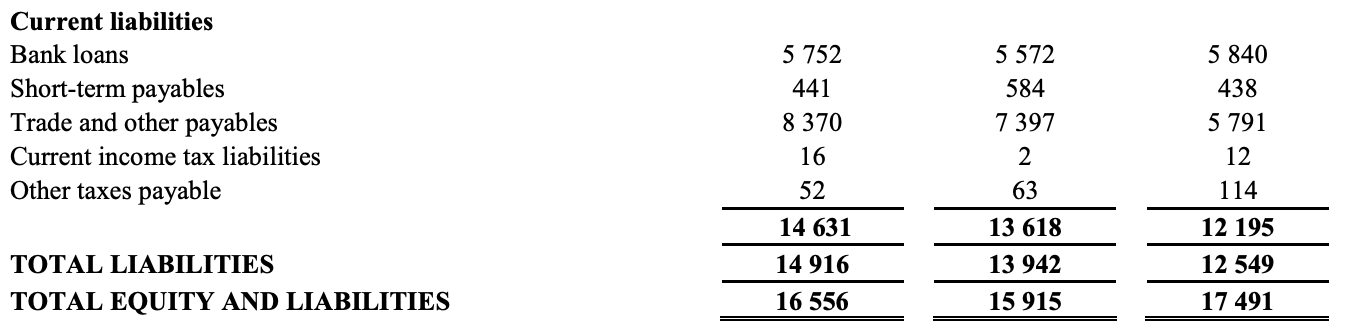

UKRPRODUCT (LSE:UKR)

Ukrproduct is a Ukrainian company focused on the production and distribution of dairy products. It has four processing plants across Ukraine where all the magic happens. To complement its product range, the company also produces beverages such as kvass and kombucha. The company has a 5-10% market share in the Ukrainian processed cheese and butter market.

Ukrproduct remains in a difficult financial situation, despite having risen an impressive +350% from its 52-week low. In the first six months of 2025, the company’s revenue was £20.2 million, which is 21.6% more than in the same period in 2024. Operating profit for the first half of 2025 was £1.218 million.

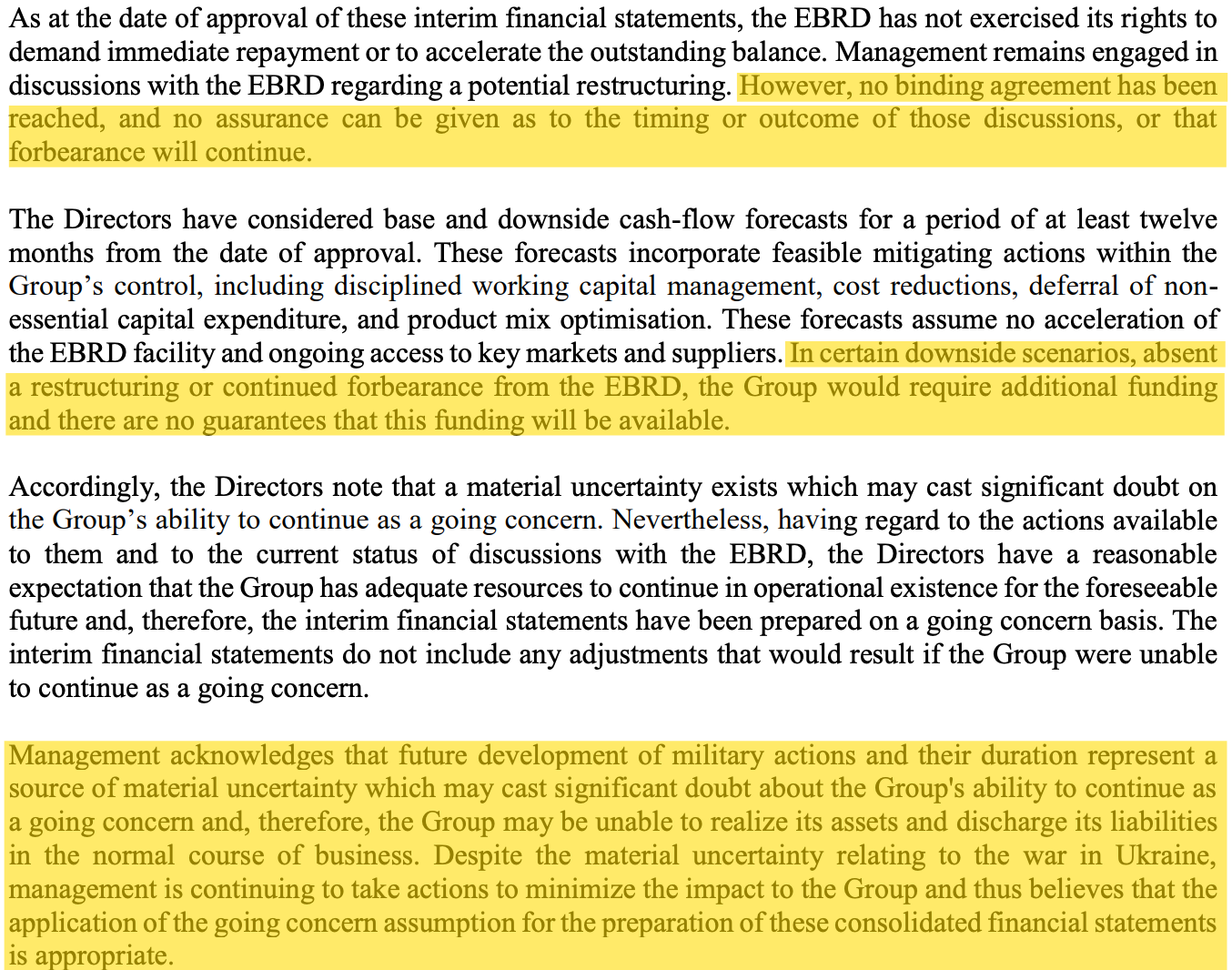

At first glance, it may seem that the company is coping well with a rising share price and profitability during these difficult times, but in the background looms the real possibility of bankruptcy. The company has £14.9 million in debt, meaning that the group is still operating under financial pressure and is still in breach of certain terms of its loan agreement with the EBRD.

So far so good, but the company’s faith remains in the hands of EBRD.

Telecommunications

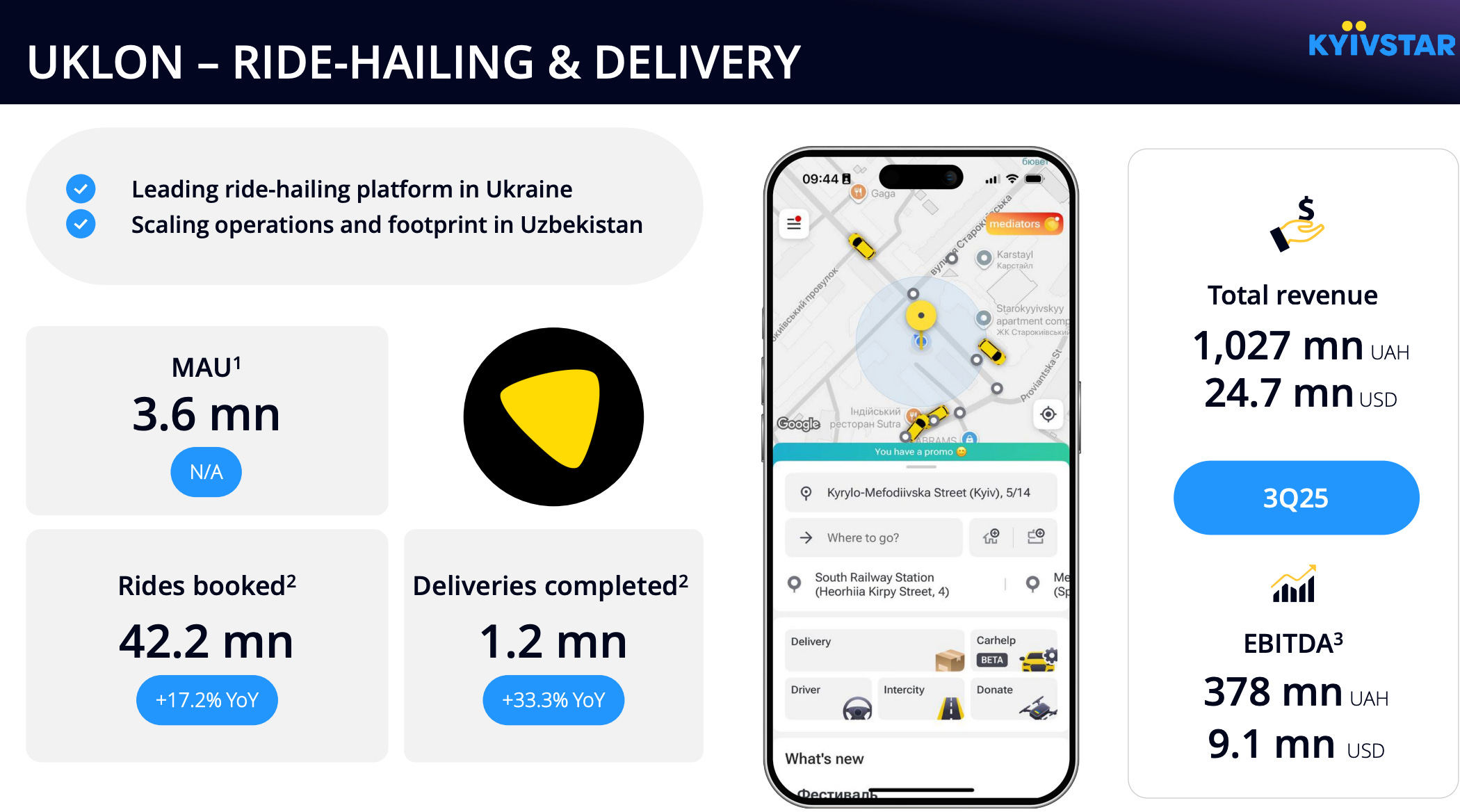

Kyivstar (NYSE:KYIV)

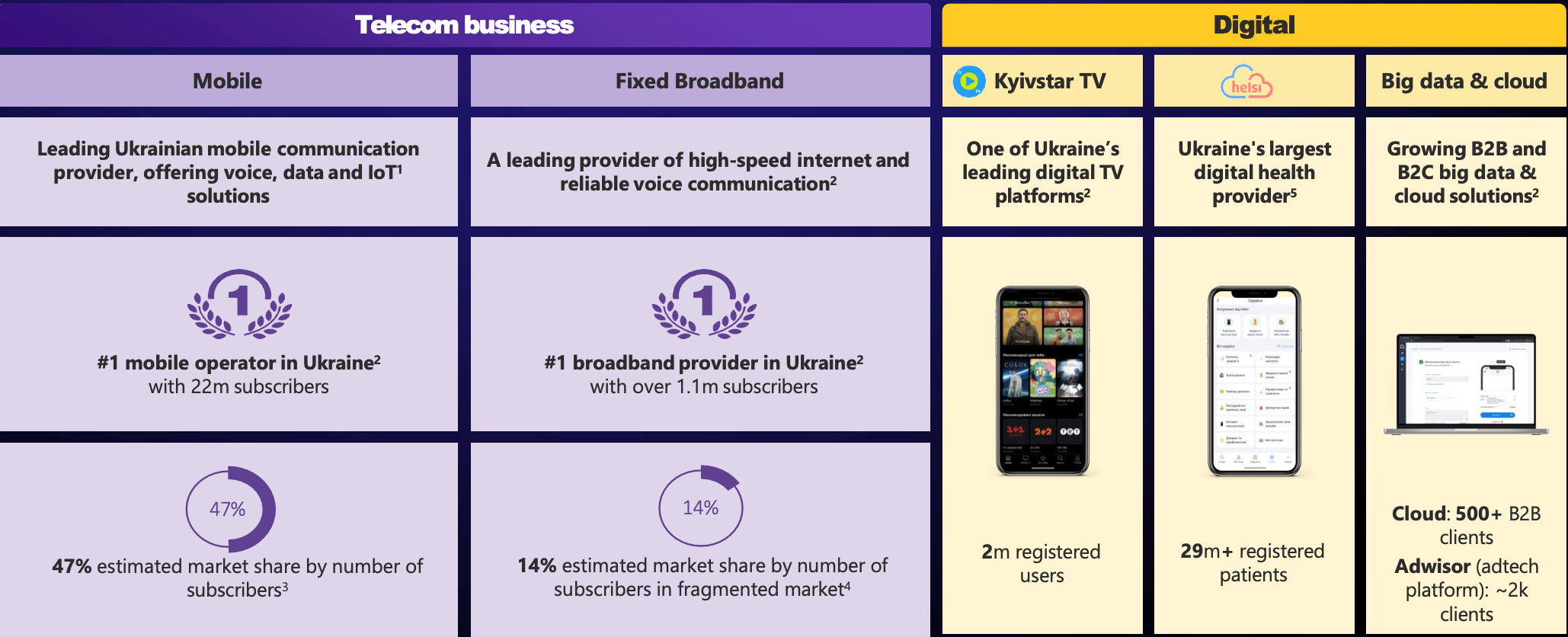

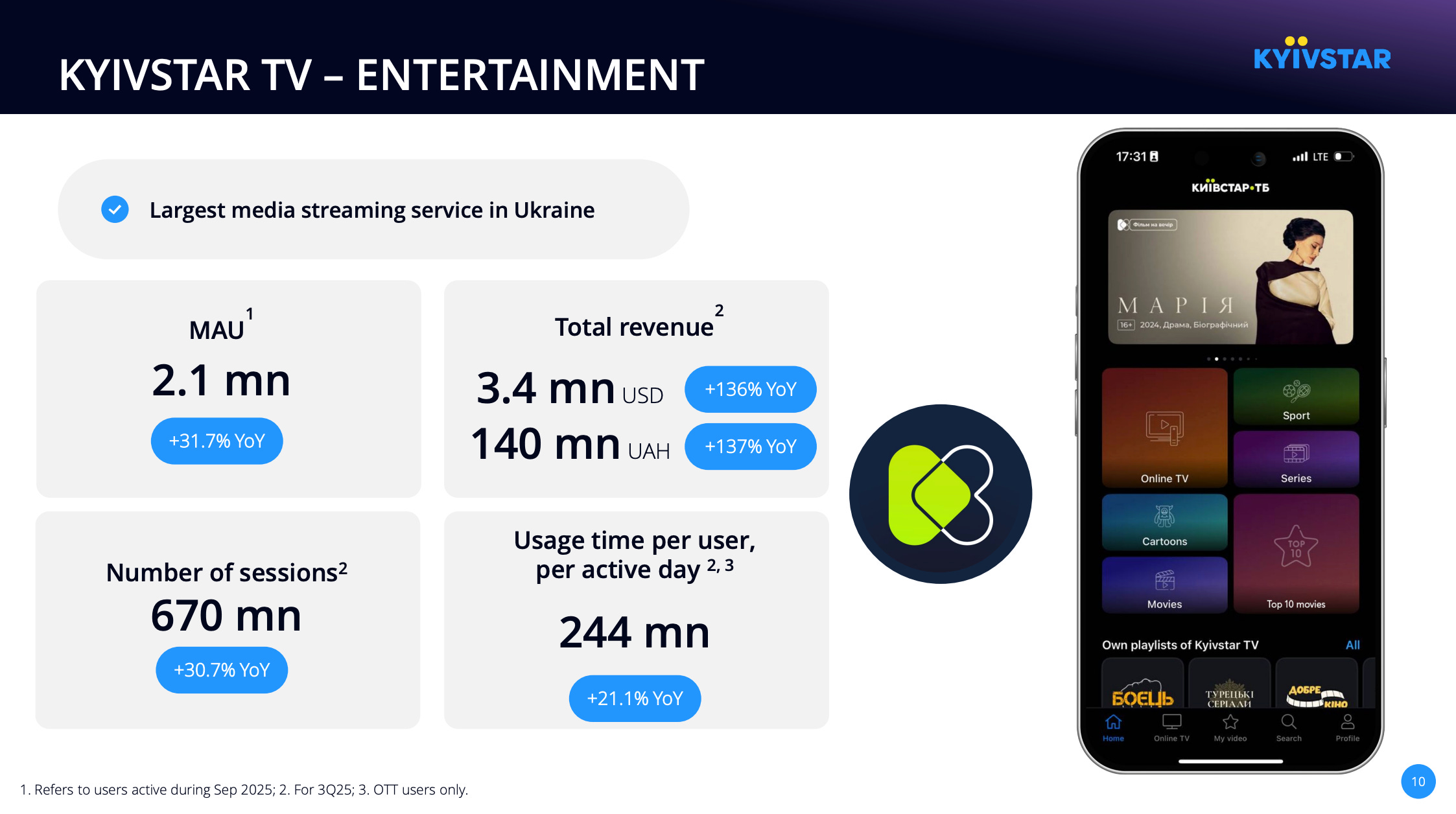

Kyivstar is the largest telecommunications operator in Ukraine, providing mobile, fixed and broadband services throughout the country, including 4G LTE and digital services. It serves over 23 million mobile users and covers 28,000 rural settlements. Its market share in the Ukrainian communications market is approximately 47%, making it the clear market leader. Kyivstar is also the only purely Ukrainian company listed on the New York Stock Exchange.

Kyivstar is also the largest digital healthcare provider in Ukraine, with over 29 million registered patients. Kyivstar is growing rapidly across multiple segments, and at first glance, the investment opportunity looks very attractive. The additional liquidity provided by Nasdaq could definitely make it a top performer if/when a permanent peace agreement is finally reached.

The company’s revenue increased by 19.8% to US$297 million in the third quarter of 2025 compared to the same period in 2024. The company has a significant cash balance of US$472 million and is committed to investing approximately US$1 billion in Ukraine by 2027.

In addition to the telecommunications business, the company have a growing business segments through media streaming, ride-hailing and deliveries, although revenues still remain small. However, the company is rapidly scaling its operations on all fronts, including ambitious goals to significantly expand its services beyond Ukraine.

Mining

Ferrexpo (LSE:FXPO)

Ferrexpo is a Swiss iron ore producer that mines, processes and exports pellets from Ukraine to Europe, Asia and the Middle East. It operates three mines and is one of the world’s largest pellet producers, controlling a significant share of the Ukrainian and European iron ore markets.

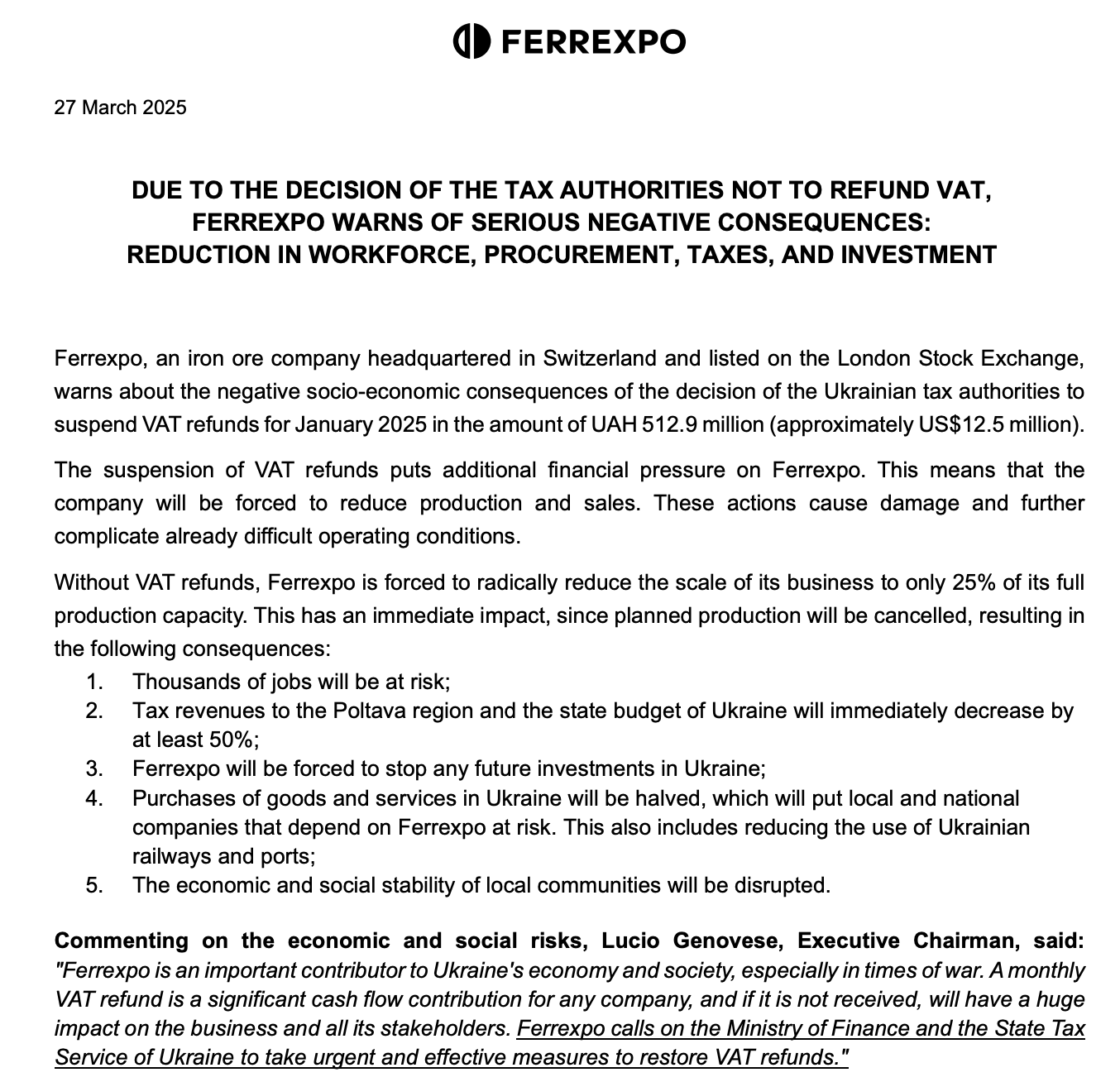

Ferrexpo has managed to keep its production running almost uninterrupted throughout the war, but the company has also been embroiled in serious disputes with the Ukrainian government. The long-running and complex disputes led to the Ukrainian government announcing in February 2025 its intention to nationalize the Poltava mine operated by the company. The mine is Ferrexpo’s largest, and by the result of the threats, its share price fell by about 50%. Naturally, Ferrexpo announced that it would take the matter to the international court, where a resolution has not yet been reached.

In addition to the threat of nationalization, the company is also fighting with the Ukrainian government over VAT; at the end of March, the company announced that the tax authorities had put VAT refunds on hold. Ferrexpo has been hit by these events hard, as at the end of the third quarter the company would have a total of $58 million in receivables that the Ukrainian tax authorities have not paid.

Ferrexpo is a major employer and taxpayer in Ukraine, but on the other side, there are also abuses of the land rights, possible connections to Russia and key personnel getting sanctioned. At this point, it is impossible to say how Ferrexpo’s story will continue—in addition to war, there is also a real risk of nationalization, large losses and liquidity issues from the VAT scandal, and other unresolved disputes.

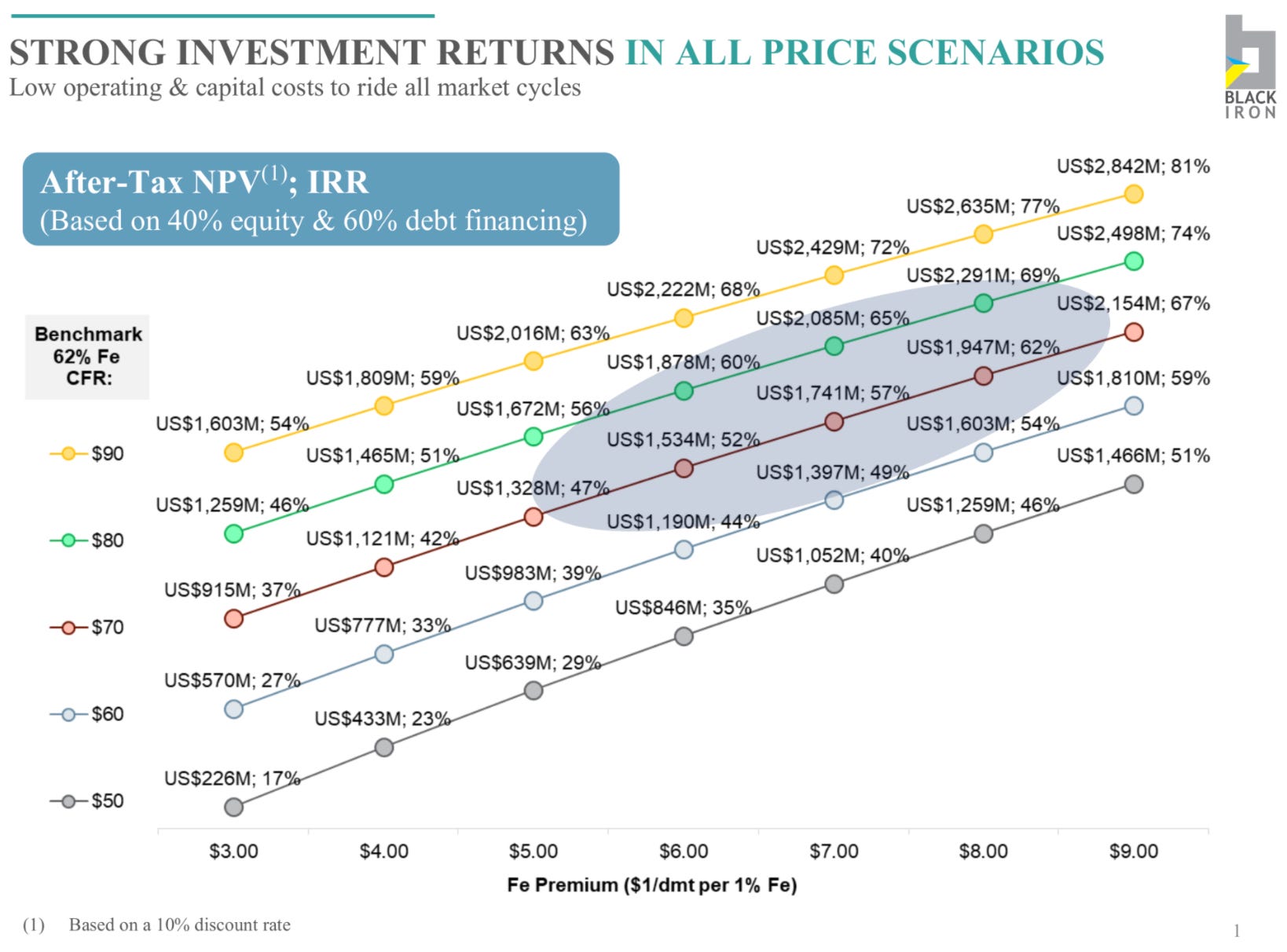

Black Iron (TSX:BKI)

Black Iron is a Canadian mining company developing the Shymanivske project in Kryvyi Rih. The area is known for its mining industry and there are other large mines nearby. Black Iron’s operations have been more or less frozen throughout the war, and the company has not been able to advance its project much.

The company’s project is significant on a global scale; the after-tax NPV10 rises to the billions in almost all price ranges, which means that there lies significant potential for a share price increase, as the company’s market value is currently around $30 million. First, of course, peace must be achieved in the country and around $450 million must be raised for the construction of the first phase, so the unwinding of the undervaluation is not that black and white.

Just days after Donald Trump’s election victory, Black Iron signed a deal with Anglo American that strengthened Black Iron’s balance sheet at a weak moment. In a swap deal in the other direction, Anglo American will get the opportunity to participate in construction funding of the project and thereby get a piece of the mine’s production for itself.

Energy

Enwell Energy (LSE:ENWE)

Enwell Energy is a fully Ukrainian-focused oil and gas company with all of its production facilities (Mekhediviska-Golotvshinska, Svyrydivske, Vasyschevskoye and Svystunivsko-Chervonolutskyi) located in the Poltava and Kharkiv regions. The company focuses on Ukraine’s growing domestic gas market, with production exceeding 2,000 barrels per day.

In 2024, the company’s revenue was $44.9 million. The company’s entire revenue comes from Ukraine. In addition to the war, the company has come under the surveillance of the Ukrainian government; Its ownership structure is questionable and the company has faced several accusations of various connections to Russia, which have led into sanctions. At the end of 2024, three of the company’s four production plants (MEX-GOL, SV, VAS) were temporarily shut down and their licenses were seized until possible connections to Russia are clarified. At the time of writing, legal proceedings are still ongoing and it is clear that the company’s profitability is suffering enormously from such extensive sanctions. As the icing on the cake, the company’s main area of operation is eastern Ukraine, which is precisely the area where the war is most intense.

Like Ferrexpo, Enwell also has its own challenges in Ukraine, which increases the company-specific risk in addition to the war. I wouldn’t necessarily play a potential peace catalyst through companies that are also under an eye of the Ukrainian authorities—in the worst case, these companies, or at least some of their holdings in Ukraine, could get nationalized.

Cadogan Energy Solutions (LSE:CADP)

Cadogan Energy is a British company that operates in western Ukraine, near the Polish and Slovak borders. The company is located in a relatively safe area, very far from the front lines.

Cadogan Energy is a very, very small company (market value about $12 million) and, in addition to Ukraine, it also has operations in Italy, where it is looking to do some exploring.

The size of the company is well illustrated by the fact that production was only 326 barrels per day in the first half of the year. The company did not reach last year’s daily result (370 barrels), due to, among other things, weakened infrastructure around the country. Revenue in the first quarter was US$3.1 million. To expand its business, Cadogan also plans to get into power generation (target 10-12MW in 2025), with the target being 10-12MW in 2025. The company has a comfortable cash pile to fund some of its new ventures ($20 million as of 30.6).

A word of caution; the London-listed stock is very illiquid and it is very typical that no trades are executed during the day.

Polish Constructors

Lets look for a few construction companies outside of Ukraine that already have a foothold in Ukraine and have been actively involved in reconstruction discussions. These companies have a main market elsewhere, which means they are not as exposed to the risks of war as their Ukrainian peers, but they can really benefit once reconstruction gets rolling.

The reconstruction of Ukraine has been estimated to cost around US$480 billion (November 2025), so there is plenty of work available for many parties.

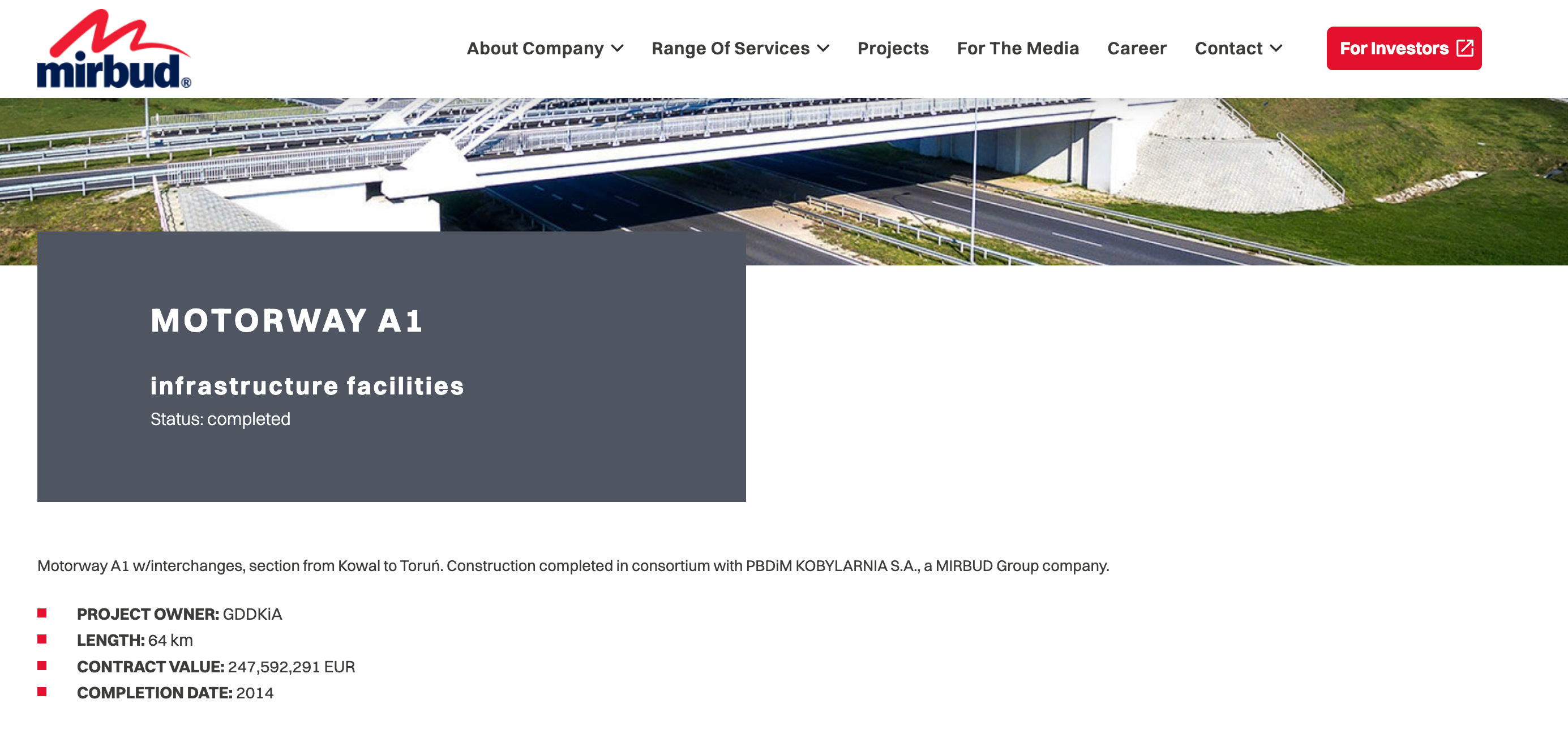

Mirbud (WSE:MRB)

Mirbud is a Polish construction company that builds apartments, public buildings, industrial halls and roads. It also owns shopping malls and produces bituminous material as a side business. The market share in the Polish construction sector is about 5%, focusing mainly on the central northern regions. The company’s website contains a convincing portfolio of the company’s various projects and, as an interesting detail, the value of the construction contract for the projects.

Just from the share price alone, it can be concluded that Mirbud’s business is rolling better than ever, even though there is a full-scale war going on in the neighboring country. Since March 2020, the share price has risen by over 2200%, meaning that the stereotypically somewhat boring construction business has returned investors’ money 23 times. Not bad!

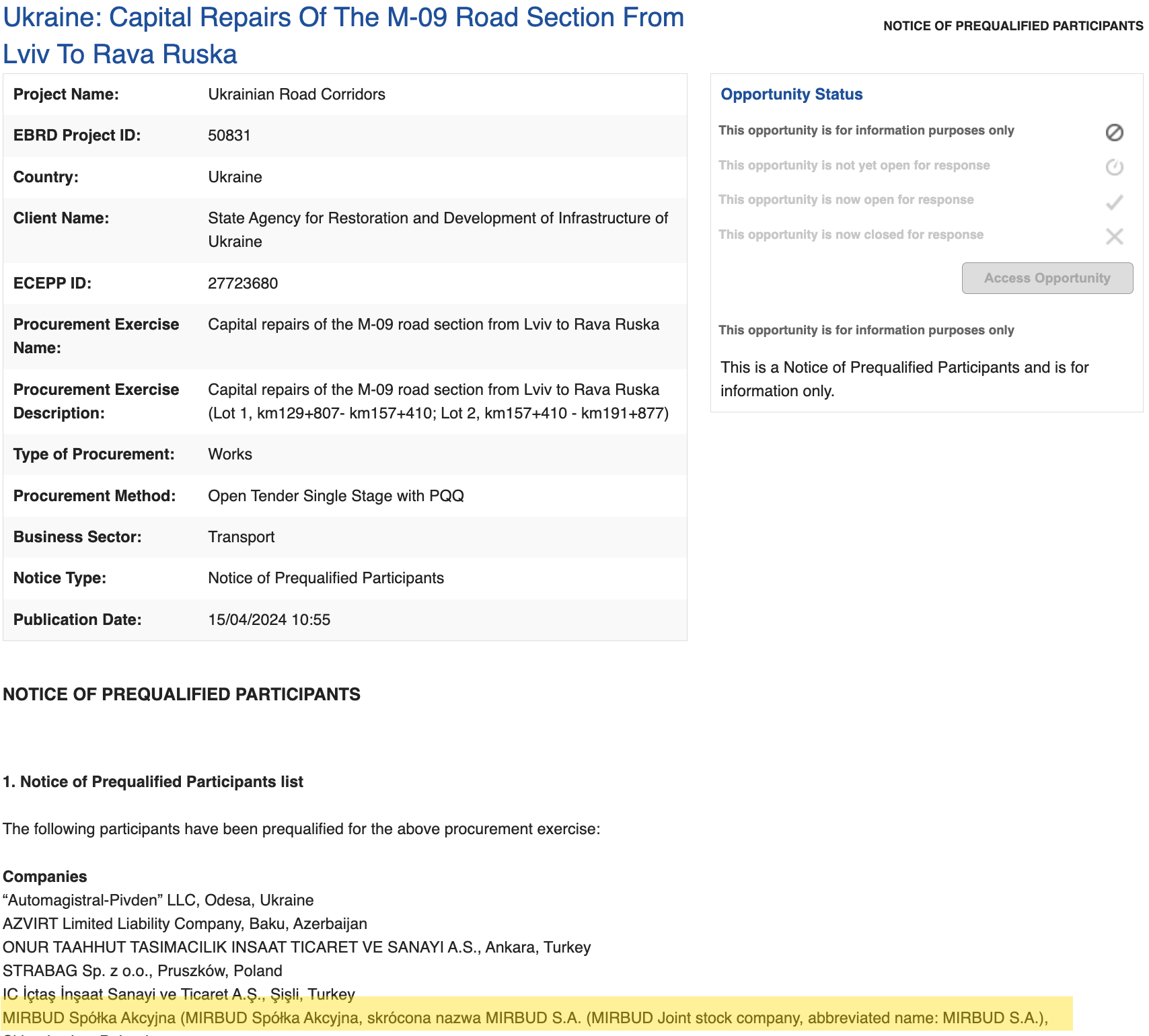

Mirbud does indeed have a foothold in Ukraine; the company first entered the Ukrainian market in 2018, and was also involved in the 2024 tender seeking a repairer for the war-torn M-09 road section from Lviv to Rava Ruska.

Budimex (WSE:BDXP)

Budimex is Poland’s largest construction company, providing general design and construction services for various infrastructure, housing, industrial projects in Poland, Germany, Slovakia and elsewhere in the EU. In Poland, it controls about 10–15% of the construction market, making it the clear market leader.

The construction boom in Poland has also sent Budimex’s shares soaring, as its price has almost sixfold increased since the coronavirus dip in 2020. The end of the war in Ukraine would certainly only increase the gains, but lets not get ahead of ourselves.

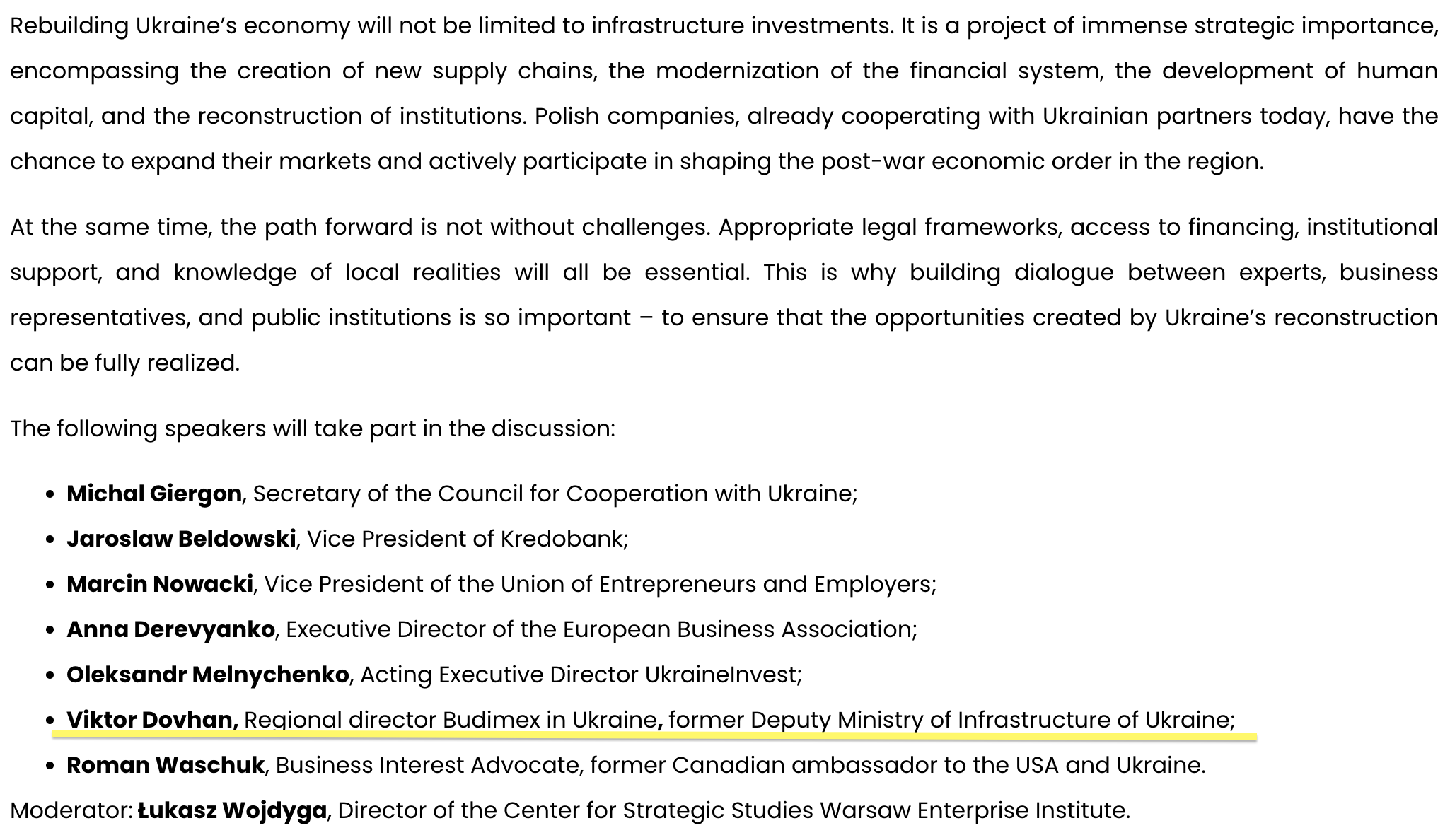

The Warsaw Enterprise Institute event held on September 12, 2025 discussed the reconstruction of Ukraine. One of the speakers was Viktor Dovhan, who also happens to the country director of Budimex in Ukraine. As the text shows, Dovhan is also a former deputy minister of infrastructure in Ukraine. Not the worst possible signing from Poland’s largest construction company. When it comes to rebuilding Ukraine, good connections with the administration are certainly worth their weight in gold.

Unibep (WSE:UNIP)

Unibep is clearly the smallest of these three construction companies in terms of market capitalization. Unibep focuses mainly on general design services for residential, public and industrial buildings. In addition to Poland’s market, the company also operates in Scandinavia, where it mainly builds modular houses with an annual capacity of around 2,000 houses. Together with buildings, the company’s portfolio also includes different road and bridge projects, which are exactly what Ukraine needs after the war.

About a month ago, Unibep signed a contract to repair and expand the Shehyni-Medyki border crossing. In addition to this contract, the company also has an active office in Lviv, Ukraine, so I think the company could be a very strong candidate to get significant construction projects in Ukraine in the future.

In June 2025, Unibep took part in negotiations to agree on a roadmap for the reconstruction of Ukraine. The company also emphasized that it has been an active player in Ukraine long before the start of the full-scale war.

Airline & travel industry

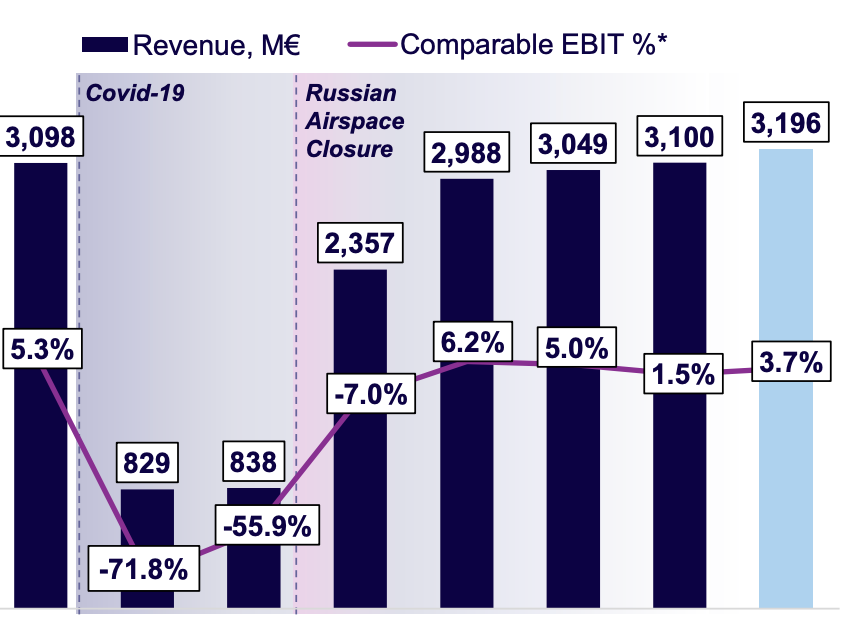

Finnair (OMXH:FIA1S)

Finnair is a Finnish flag carrier, which unfortunately has had a very difficult decade so far. Everybody know how coronavirus affected travelling, but especially foreigners are probably not aware that Finnair basically lost their competitive advantage because of Russia-Ukraine war. So, that is two, not only major, but prolonged negative events in the span of few years in a sector which is really competitive.

What was that competitive edge I was talking about then? Well, before the full scale invasion in 2022, Finnair was able to use Russia’s airspace to fly directly, fast and cheaply to various Asian destinations, but due the war, the airspace is now closed and Finnair has to make a detour around Russia. And that is a long detour to make…

Finnair has updated its strategy for 2026-2029 and the consensus is that the Russian airspace will remain closed. If that airspace ever opens up again, Helsinki-Vantaa airport as Finnair’s hub, which is geographically well-suited for connecting Europe and Asia would probably drive Finnair into new heights. In example, every Helsinki-Tokyo flight is now approx. 2 hours longer because you have to detour around Russia.

In my opinion airlines in general are not attractive businesses to invest in, and it is also important to note that the Government of Finland is the biggest shareholder of Finnair, as it owns around 55% of the shares. Government ownership is rarely a good thing, as it usually stalls the progress and the key hirings could be more based on politics rather than pure skill and suitability.

You also need to take into account, that even if the war eventually stops, there are no guarantees that the Russian airspace will open or that Finnair wants to return into the old. If the peace or ceasefire is being reached, I think this would be a crowded trade here in Finland, but I’m personally more interested about companies who have direct exposure to Ukraine.

The end

If you read until the end, thank you! Here is my small reward for you; A cheat sheet with key economic numbers from all 17 companies.

Hopefully you find this article useful and you found some interesting companies from the list. And of course, remember to do your own due diligence, as there are certainly some rotten eggs in the basket.

can you find a single statement from Russian officials about a "3 day operation"?